Should an FTTH Operator Choose a Retail, Wholesale, or Open-Access Model?

Choosing the wrong business model for your fiber network is one of the most expensive mistakes an FTTH operator can make — and most teams don’t realize it until they’re already three years into deployment.

In the retail vs wholesale FTTH debate, there’s no universal winner. Each model carries distinct revenue logic, risk exposure, and competitive implications. The right choice depends on your market position, capital structure, and long-term ambitions.

Get it right, and your infrastructure becomes a compounding asset. Get it wrong, and you’re left with stranded assets and a take-rate that won’t cover your WACC.

This post breaks down all three models — retail, wholesale, and open-access — so you can make a strategic decision backed by data, not industry folklore.

The Stakes Are Higher Than You Think

According to the FTTH Council Europe’s 2024 Market Overview, Europe alone passed 280 million homes with fiber — yet household penetration in many markets still sits below 50%. That gap isn’t just a marketing problem. It’s often a structural one: operators chose a business model that limits their ability to monetize the network they built.

Meanwhile, the ITU’s Broadband Commission consistently highlights that open-infrastructure models accelerate adoption in competitive markets. The question is whether those models work for your specific situation.

Let’s dig in.

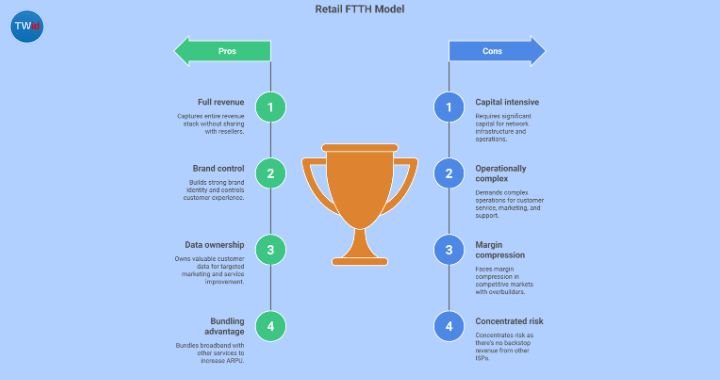

The Retail FTTH Model: Control, Margin, and Risk

In a retail model, you own the network and serve the end customer directly. You’re the ISP. You handle billing, customer service, marketing, and the whole subscriber relationship.

Why operators choose it

The appeal is obvious: you capture the full revenue stack. No sharing, no margin compression from resellers. You build your brand, own the data, and control the customer experience end-to-end. For markets where you have strong brand equity or first-mover advantage, the retail model is extremely powerful.

Operators like AT&T Fiber in the US and Swisscom in Switzerland have made this work at scale. Their ability to bundle broadband with mobile, TV, and smart home services creates an ARPU story that pure-infrastructure players simply cannot replicate.

If you’re growing ARPU without increasing churn, bundling under a retail model is often the most direct path.

The downside

Running a retail operation is capital and operationally intensive. You need a customer acquisition engine, a churn management function, a 24/7 support center, and the working capital to fund subscriber growth before you start collecting recurring revenue. In a competitive market — especially one where overbuilders are entering your footprint — margin compression hits hard.

The retail model also concentrates risk. If your take-rate disappoints, there’s no backstop revenue from other ISPs using your network.

The Wholesale FTTH Model: Scale Fast, Share the Revenue

In a wholesale model, you build and operate the passive or active network infrastructure, then lease capacity to one or more retail ISPs. You’re in the infrastructure business, not the subscriber business.

Why it’s gaining traction

The economics are increasingly attractive. You de-risk your revenue by spreading it across multiple service providers. Even if one ISP underperforms, others on your network are still generating traffic and paying access fees. This model is particularly compelling for infrastructure investors — PE firms and pension funds love the predictable, long-duration cash flows.

Countries like the Netherlands have thrived under a quasi-wholesale model. Companies such as Reggefiber (now part of KPN) and independent altnets have demonstrated that institutional capital is far more accessible when the network is positioned as infrastructure rather than a consumer brand.

There’s also a speed advantage. When you’re not building a retail operation in parallel, you can deploy fiber faster. That matters enormously when you’re racing to increase take-rate in homes passed before a competitor locks in the addresses.

The tradeoff

You lose direct customer control and full revenue upside. Your wholesale pricing needs to be competitive enough to attract ISPs but sustainable enough to service your debt and deliver investor returns. Negotiating long-term anchor tenant agreements before you break ground is critical — a wholesale model without committed offtake is a very uncomfortable position.

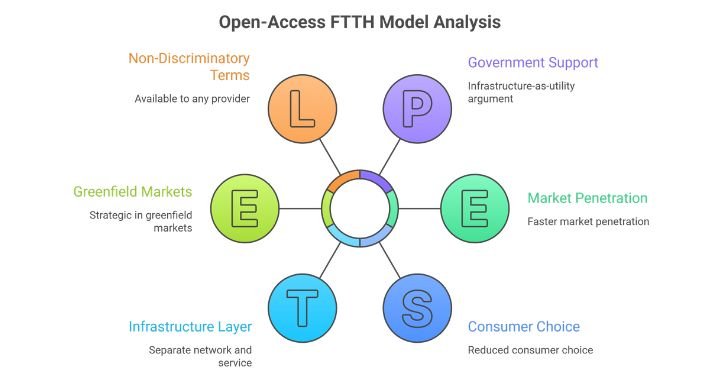

The Open-Access Model: Maximum Competition, Maximum Coverage

Open access takes the wholesale concept further. Your network is designed from day one to be available to any licensed service provider on non-discriminatory terms. No exclusivity, no preferred partners — open to all.

The infrastructure-as-utility argument

Australia’s NBN Co is the most cited example globally. Built as a government-backed open-access network, it was explicitly designed to prevent incumbent monopoly. The model worked for coverage (nearly universal), though it’s had well-documented challenges with pricing structures and wholesale rate disputes that reduced ISP margins and, in turn, consumer choice.

More refined open-access models are emerging in Sweden, Denmark, and Singapore, where the infrastructure layer is kept strictly separate from the service layer. IDATE DigiWorld research consistently shows that functional or structural separation of network and service layers correlates with faster market penetration in competitive urban areas.

When open access makes sense

If you’re a municipal network, a utility company entering fiber, or a first-time infrastructure investor without a retail brand, open access can be your fastest route to relevance. You’re not trying to win the retail war — you’re trying to make the infrastructure indispensable.

It also works strategically in greenfield markets where no incumbent has footprint. Getting three or four ISPs to commit to your open-access platform before launch creates a far stronger business case for debt financing than a single-ISP retail launch.

Retail vs Wholesale FTTH: Side-by-Side Comparison

| Dimension | Retail | Wholesale | Open Access |

|---|---|---|---|

| Revenue ownership | Full stack | Infrastructure only | Infrastructure only |

| Customer relationship | Direct | Indirect | Indirect |

| Revenue predictability | Moderate | High (with anchor tenants) | High (diversified) |

| Capital intensity | Very high | High | High |

| Time to first revenue | Slower | Faster | Fastest |

| Brand building | Strong | None | None |

| Regulatory complexity | Moderate | Low–Moderate | Can be high |

| Best for | Incumbents, branded altnets | Infrastructure funds, neutral hosts | Municipalities, utilities, greenfield markets |

How to Choose: Three Questions Every Executive Should Answer

Rather than defaulting to what competitors do, use these three diagnostic questions to pressure-test your model choice.

1. What is your primary capital constraint?

If you’re equity-light and dependent on debt or infrastructure funding, wholesale or open access will typically attract better terms and valuations. Lenders and infrastructure funds price retail customer risk very differently from infrastructure cash flows. If you’re well-capitalized with a consumer brand, retail may generate better long-run equity returns.

2. How competitive is your target market?

In markets with two or more existing broadband providers, a retail entry is a fight for market share with high customer acquisition costs. Wholesale or open access positions you above the competitive fray. In underserved or rural markets with no incumbent fiber, retail can be highly profitable with limited competition.

3. What’s your 10-year exit or evolution strategy?

Infrastructure-only models tend to attract strategic acquirers and institutional capital at higher multiples. Retail ISPs are valued differently — on EBITDA and churn metrics rather than asset value. If an infrastructure sale or IPO is in the plan, your business model architecture matters enormously for valuation.

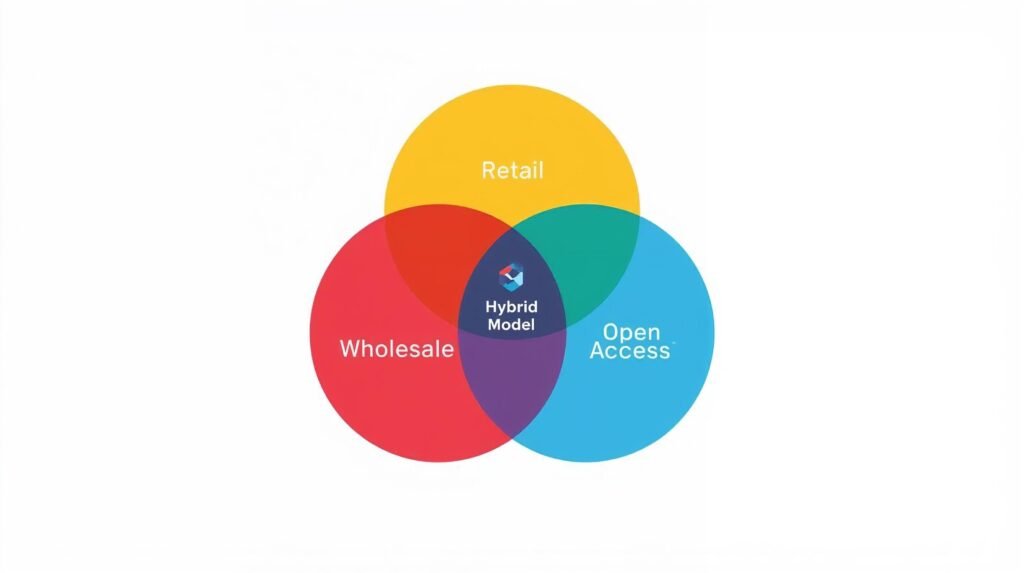

Hybrid Models: The Best of Both Worlds (With Caveats)

Many operators are increasingly running hybrid approaches — owning the passive network and offering it on wholesale terms while also operating a retail brand. This isn’t new (BT Openreach in the UK is the most famous example), but the operational complexity is real. You need genuine Chinese walls between your retail and wholesale teams, or your wholesale partners will not trust the arrangement.

Done well, hybrids maximize revenue and preserve competitive optionality. Done poorly, they create regulatory exposure and destroy wholesale relationships.

Frequently Asked Questions

1. What is the difference between a wholesale and an open-access FTTH model?

In a wholesale model, the infrastructure owner selects and contracts with one or a few retail ISPs to use the network. There may be exclusivity or preferred pricing arrangements. In an open-access model, the network is available to any licensed service provider on equal, non-discriminatory terms — no exclusivity allowed. Open access is essentially wholesale with a stricter neutrality requirement.

2. Which FTTH business model generates the highest ARPU?

The retail model typically generates the highest ARPU per subscriber because the operator captures the full service revenue — broadband, TV, mobile bundles, and value-added services. However, wholesale and open-access models can generate competitive returns on invested capital (ROIC) because their cost structures are leaner and their revenue is more predictable.

3. Can a small altnet viably run a retail FTTH model?

Yes, but it’s operationally demanding. Small altnets that succeed in retail typically focus on a tight geographic footprint, differentiate on service quality rather than price, and keep overhead lean. Many eventually shift toward a wholesale or hybrid model as they scale, because the economics become more attractive for capital recycling and exit optionality.

4. How does the choice of FTTH business model affect access to infrastructure financing?

Infrastructure funds and pension capital strongly prefer wholesale or open-access models because the revenue profile resembles utility cash flows — long-term, contracted, and not dependent on consumer churn dynamics. Retail FTTH operators typically access financing through different channels: bank debt, strategic equity, or operator-backed capital. The model choice directly shapes your investor universe.

5. Is the open-access model always regulated, or can it be voluntary?

Open-access can be either. In some markets (Australia’s NBN, Sweden’s municipal networks), it’s mandated by regulation or government policy. In others, operators voluntarily adopt open access as a competitive strategy — to attract ISP partners, access public subsidy programs, or differentiate from vertically integrated incumbents. Voluntary open access is growing in markets where neutral host positioning creates a genuine commercial advantage.

The Bottom Line

The retail vs wholesale FTTH decision is ultimately a bet on where you create the most value — at the infrastructure layer or the service layer. Both can generate excellent returns. Both carry real risks. The operators who struggle are those who pick a model without fully pressure-testing it against their capital structure, competitive environment, and long-term strategy.

Be honest about your strengths. If you have a consumer brand, go retail and defend it aggressively. If you have infrastructure capital and no desire to run a call center, build the best wholesale platform in your market. If you’re a municipality or utility, open access may be the fastest path to ubiquitous coverage and stakeholder trust.

Whatever you choose — commit to it architecturally from day one. Retrofitting a retail network into an open-access platform mid-deployment is one of the most expensive lessons in fiber infrastructure.

Ready to sharpen your FTTH content and thought leadership strategy? Explore how professional FTTH ghostwriting can help you turn complex operational insight into compelling executive content that opens doors.

Joen — TheWriter.id

Specialized ghostwriter for the FTTH and Telecommunications industry. I help ISPs, network architects, and telecom vendors translate technical complexity into executive-level business value.

joen@thewriter.id →