Fiber Cost Per Home Passed: 2026 Executive Benchmarks & Calculator

Written by Junun Saleh

·6 min read·Updated May 2026·FTTH Economics

Cost per home passed rises as housing density falls – the core economics behind every fiber build decision.

Cost per home passed is one of the fastest ways to judge whether a fiber build is financially realistic. For executives, it turns engineering scope into a capital decision: where to build, how much to invest, and what take rate is required for the project to work.

The headline is simple: density drives the economics. A dense urban mile can spread construction cost across many homes. A rural mile may require similar network investment but serve only a handful of locations. That difference can move the business case by 10x.

This executive guide summarizes the 2026 planning benchmarks, the distinction between homes passed and homes connected, the main cost pressures, and the take-rate math management teams need before approving capital.

Executive summary

Use $18/ft underground and $8/ft aerial as current FBA benchmark medians for labor and materials. In per-home terms, dense urban projects can sit near $1,000 per home passed, while rural and remote builds can reach $8,000-$20,000+. The national blended average is closer to $1,000-$1,500 because most passings are in denser markets. Customer drops are separate and typically add about $340-$680 per connection before ONT and activation costs.

What Management Needs to Separate

Most fiber cost confusion comes from mixing two different metrics. They answer different business questions:

Cost per home passed (CPHP) – the network build cost divided by the number of serviceable homes along the route. It measures capital efficiency before any customer signs up.

Cost per home connected (CPHC) – the cost once a customer subscribes, including the drop, equipment, and truck roll. It measures the effective cost to acquire and activate a paying customer.

Homes passed is a network investment metric. Homes connected is a revenue conversion metric. Executives should review both before approving a build, because a low CPHP can still underperform if take rate is weak.

2026 Benchmarks for Capital Planning

The FBA/Cartesian 2025 report shows median construction cost per foot by density tier. The table below is the clean starting point for executive planning: method, density, and route length determine the capital requirement.

Build environment

Homes / route mile

Underground (median $/ft)

Aerial (median $/ft)

Urban / densely populated

>50

$20.38

$9.00

Suburban

11 – 50

$17.00

$7.10

Rural

5 – 10

$15.00

$5.47

Extremely rural

< 5

$11.88

—

Median cost per foot, labor and materials only, by the report’s own housing-density definitions (FBA/Cartesian 2025, Figure 2.7). The aerial figure for extremely rural is omitted — the report had limited data for that tier.

The important management insight is that dense areas may cost more per foot but less per home, because each route mile reaches more potential customers. Rural builds may look cheaper per foot and still be far more expensive per home.

As a planning shortcut, $18/ft underground equals about $95,000 per route mile before soft costs. Aerial construction at $8/ft is closer to $42,000 per route mile. Divide either number by homes per mile, then add engineering, make-ready, permitting, and other project costs. The FBA report indicates deployment labor and materials are only about 55% of total project cost.

That is why a blended $1,000-$1,500 national average can be misleading. It reflects the fact that many passings are in denser markets. Rural projects need their own investment logic, often including grants, subsidies, or strategic coverage obligations.

Executive takeaway

A high rural cost per home passed is not automatically a bad project. It may be the correct number for the territory. The real question is whether the funding mix, take rate, ARPU, and strategic value support the investment.

Clear communication matters because boards, investors, and grant reviewers fund the story they can understand.

From Cost Per Foot to Cost Per Home Passed

The conversion is straightforward: multiply cost per foot by 5,280 feet, then divide by homes per mile. The table below shows why density changes the investment case faster than construction method alone.

Density tier (FBA)

Published $/ft (UG)

Homes / mile

Per route mile

Cost per home passed

Urban

$20.38

100

$107,606

$1,076

Suburban

$17.00

30

$89,760

$2,992

Rural

$15.00

8

$79,200

$9,900

Extremely rural

$11.88

3

$62,726

$20,909

Cost per home passed = the report’s published per-foot median × 5,280 ÷ homes per mile (underground, labor and materials). Homes-per-mile is the only assumed input, shown at a representative value within each FBA density band; engineering, make-ready, and permitting add ~45% on top.

The management point is simple: rural construction can cost less per foot and still be much harder to finance. Density usually has more impact on the final business case than the headline construction rate.

Cost-Per-Home-Passed Calculator

Live · No signup

Enter your route miles, density, build method, expected take rate, and drop cost. The calculator translates construction scope into cost per home passed, cost per connected customer, and total capex for management review.

Cost per home passed

$915

Cost per home connected (all-in)

$2,668

Total project capex

$9.3M

Homes passed

7,500

Homes connected

3,488

Network build cost

$6.9M

Run the numbers above to see where this build sits.

If current contractor quotes are higher than older planning assumptions, the issue is usually market pressure rather than one bad bid. Management teams should watch five cost drivers:

Labor and materials. Labor is the largest cost component, representing about 72% of underground and 64% of aerial deployment in the FBA 2025 data.

Permitting delays. Delays extend schedules, tie up crews, and push project cash flow later than planned.

Make-ready work. Pole attachments, utility coordination, and route changes can materially change aerial build economics.

Terrain and method. Rock, trenching, boring, plowing, and mixed construction methods can move per-foot cost significantly.

Lower-density expansion. Many remaining unserved or underserved areas have fewer homes per road mile, which raises cost per home passed by design.

Take Rate: The Metric That Converts Capex Into Revenue

A passed home does not generate revenue until it subscribes. Take rate is therefore the bridge between network capex and customer economics.

At a 46.5% take rate, a $1,000 cost per home passed becomes roughly $2,150 in network cost per paying customer before the drop. That is the number leadership should compare against ARPU, margin, churn, payback period, and lifetime value. Improving retention and ARPU can materially improve returns on capital that has already been spent.

Aerial vs. Underground: The Board-Level View

Aerial builds are usually faster and materially cheaper per foot, but they carry exposure to pole access, make-ready delays, and weather risk. Underground builds cost more but can improve durability, aesthetics, and competitive defensibility. Most real-world projects blend both methods based on route conditions.

How Leadership Should Use This Number

Cost per home passed should appear in three decision documents: the investor model, the board deck, and the grant or BEAD narrative. In each case, the number must answer the same question: does this territory justify the capital when density, take rate, customer value, and funding support are considered together?

Make the investment case clear

Strong fiber economics still need a clear executive narrative.

I help ISPs, telco operators, and network vendors translate technical build data into language that boards, investors, management teams, and grant reviewers can act on.

Board and investor narratives that explain why a build deserves capital

BEAD and grant applications where the cost story is easy to evaluate

Executive content that makes network economics clear to non-technical buyers

Custom calculators and decision tools built around your own assumptions

For executive planning, use roughly $1,000 per home passed in dense urban builds, about $3,000 in suburban builds, and $8,000-$20,000+ in rural or remote markets. The range is wide because density changes how many homes share each route mile of construction.

Does cost per home passed include the customer connection?

No. Cost per home passed covers the route network that passes a serviceable home. The customer drop, ONT, truck roll, and activation work are separate costs that apply when a home actually subscribes.

Why is rural fiber more expensive per home passed?

Rural routes have fewer homes per mile. Even if the construction cost per foot is lower, the cost is divided across fewer potential customers, which increases the per-home number.

How does take rate affect the investment case?

Take rate determines how many passed homes become paying customers. At a 46.5% take rate, the effective network cost per connected customer is roughly double the cost per home passed before drop and activation costs.

What is a good cost per home passed?

There is no single good number. Dense urban projects below about $1,200 per home passed can be attractive, while rural projects may require $8,000-$16,000 per home passed and still make sense with grants, subsidies, or strategic coverage goals.

Sources & Methodology

Fiber Broadband Association & Cartesian — 2025 Fiber Deployment Cost Annual Report (38-state survey; $18/ft underground & $8/ft aerial 2025 medians; labor 72%/64% of deployment; deployment ≈ 55% of total project cost; underground drops $556–$675, aerial $338–$400; 92% saw higher costs in 2025, 88% expect increases in 2026; fiber won 63% of BEAD-eligible locations and 84% of awarded funding).

Figures are planning ranges synthesized from public 2024-2026 data and current cost trends. Validate all assumptions against local contractor quotes, permitting conditions, take-rate expectations, and financing requirements before committing capital. Educational content, not investment advice.

Open Access FTTH Model vs Retail FTTH: Which Business Model Creates More Long-Term Value?

Most fiber executives don’t get to choose their business model twice. Once you’ve committed billions in CapEx to a retail or open access FTTH model, unwinding that decision mid-deployment is one of the most expensive mistakes in the industry.

And yet, the choice between open access and retail FTTH is often made too early, too quickly, and without enough financial modeling behind it. The result? Stranded assets, underwhelming take-rates, and a network that never reaches the utilization levels needed to justify its cost of capital.

This post breaks down both models — not from a textbook perspective, but from the standpoint of long-term value creation. We’ll look at what the data actually says about revenue yield, investor sentiment, and competitive resilience so you can make a strategic decision that compounds over the next two decades.

Understanding the Two Models: Structure Shapes Everything

Before comparing outcomes, it’s worth being precise about what we’re comparing.

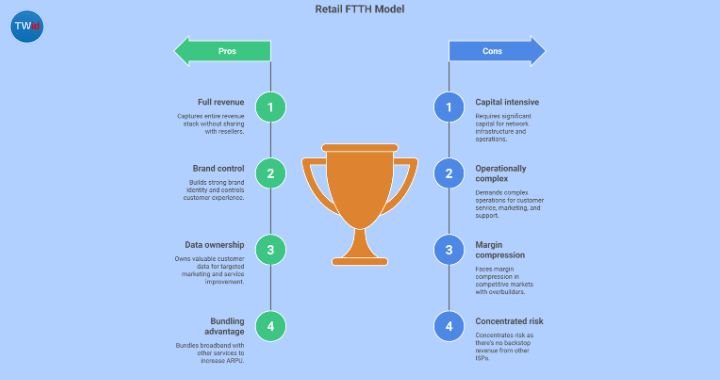

Retail FTTH is the vertically integrated model. The operator builds the fiber infrastructure, manages the network, and sells broadband services directly to end customers. Everything — from CapEx to customer service calls — sits on one balance sheet. Revenue comes from monthly subscriptions, and the operator competes for customers against every other provider in the market.

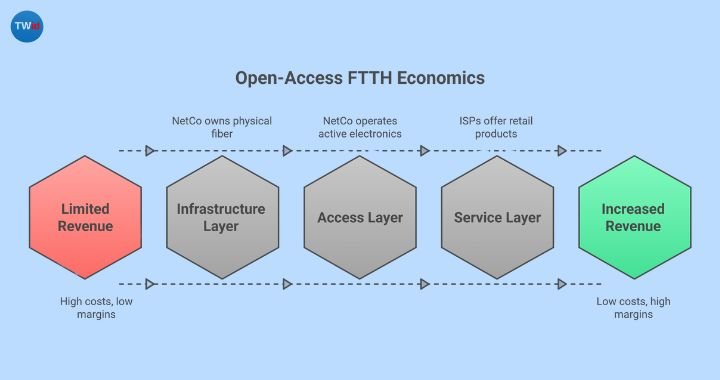

Open access FTTH separates infrastructure from service delivery. A network company (often called a NetCo) builds and operates the fiber plant, then opens it to multiple internet service providers who compete on that same network. Revenue for the NetCo comes from wholesale access fees per activated subscriber, potentially supplemented by dark fiber leases and enterprise connectivity.

The structural distinction is simple. The financial consequences are not.

If you’re weighing the merits of retail, wholesale, and open access models in more detail, this breakdown of how each FTTH business model shapes competitive strategy is a useful starting point before diving into valuation math.

The Open Access FTTH Model: Where the Utilization Math Shifts

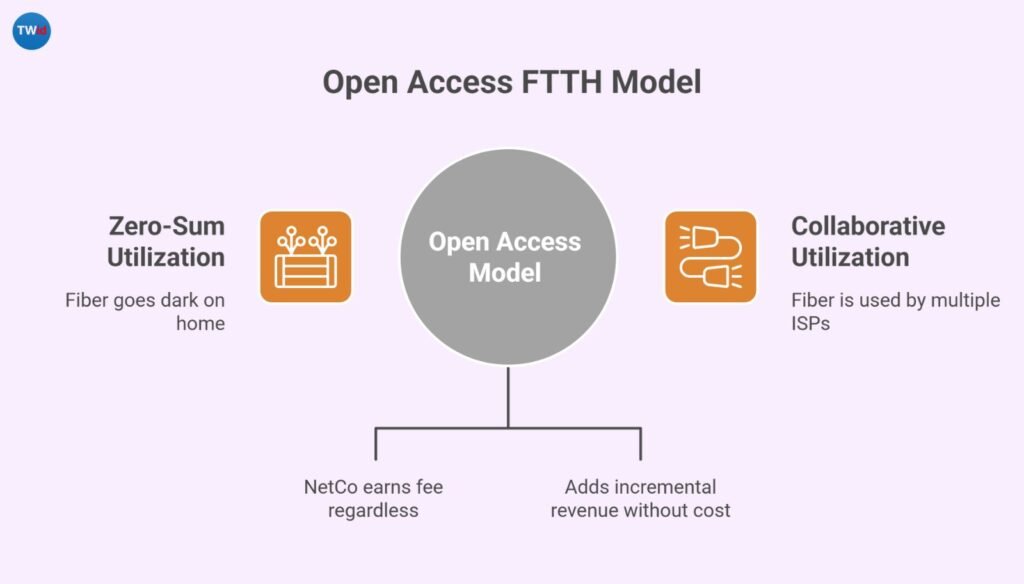

Here’s the core economic argument for the open access FTTH model: it changes the utilization equation from zero-sum to collaborative at the infrastructure level.

In a retail model, if a customer picks a competitor on a different network, your fiber goes dark on that home. You either win the subscriber or earn nothing. In an open access model, the customer might choose a different ISP — but they’re still running over your fiber. The NetCo earns a wholesale fee regardless of which retail brand the customer prefers.

The take-rate implications are significant. Open access networks with multiple ISPs have reported take-rates as high as 70% to 90%, compared to the 30% to 50% range that’s typical for single-provider networks in competitive urban markets. That gap matters enormously when you’re trying to generate returns on capital-intensive infrastructure.

Each additional ISP on the platform adds incremental revenue without proportional incremental cost. The marginal economics are compelling — which is exactly why institutional investors have started paying attention.

The Retail Model: Higher Margins Per Subscriber, Higher Concentration Risk

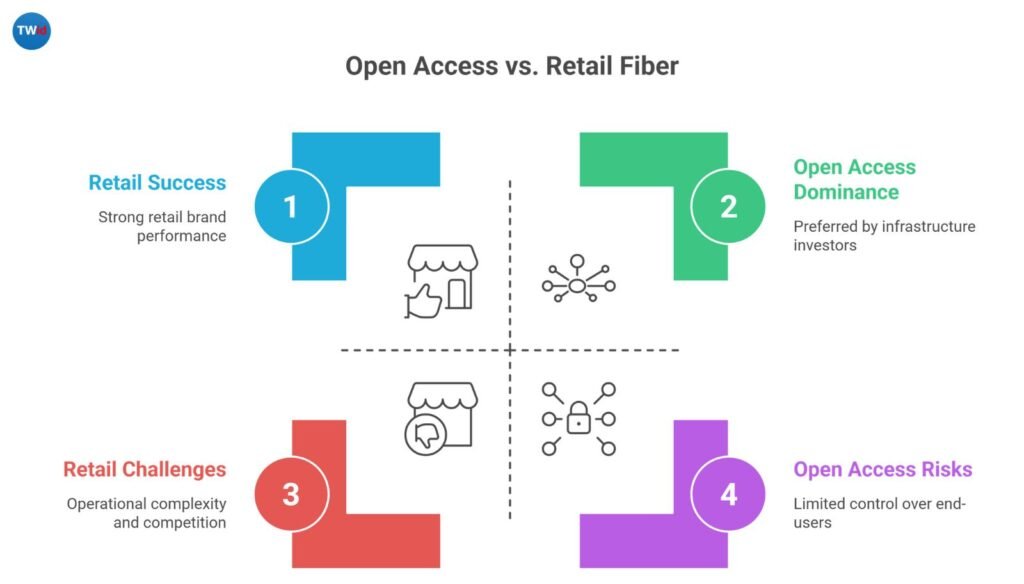

The retail model isn’t without advantages. When it works, per-subscriber margins are higher because the operator captures the full revenue stack — infrastructure fees plus retail pricing. There’s no wholesale discount eating into the economics.

For operators with strong consumer brands, established distribution channels, and the operational muscle to manage customer acquisition and churn at scale, retail can be a powerful model. You own the customer relationship. You control pricing. You dictate the service experience end to end.

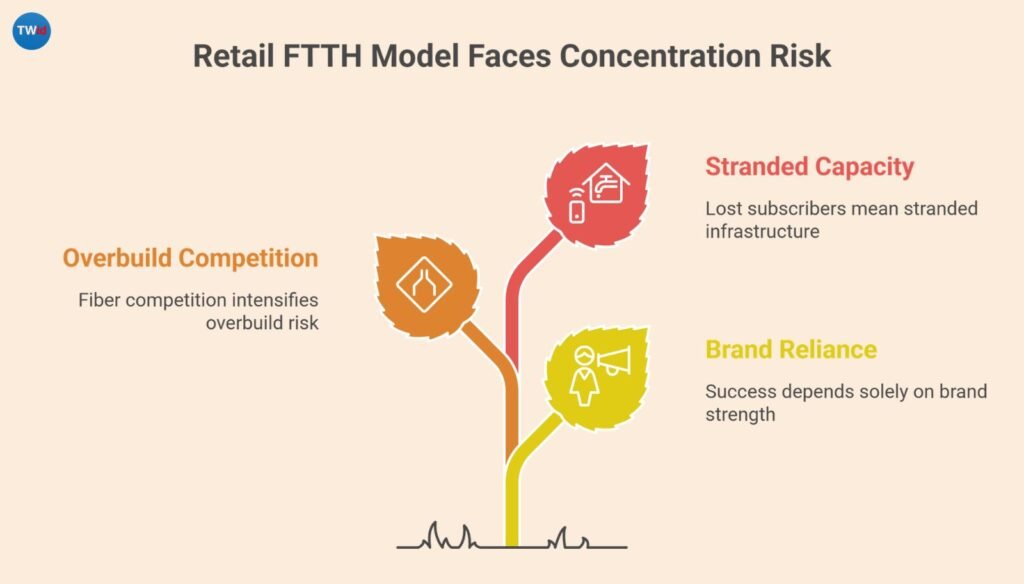

But the risk profile is different.

Retail FTTH operators carry concentration risk. You’re betting that your brand alone can sustain enough take-rate to justify the infrastructure investment. In markets where overbuild is increasing — and it is, with fiber competition intensifying rapidly in many regions — that bet becomes harder to win. As EY reported, return minimums for FTTH builds have risen from the 8-10% range in 2021-2022 to 12-15% today, largely driven by higher interest rates and growing competitive overbuild risk (source).

When your only path to monetizing each home is winning the retail customer, every lost subscriber is stranded capacity.

What Investors Actually Prefer — And Why It Matters

Here’s where the valuation gap gets real.

Infrastructure funds, pension capital, and private equity firms have increasingly signaled a preference for wholesale and open access fiber models. The reason is structural: open access revenue profiles resemble utility cash flows — long-term, contracted, and diversified across multiple tenants. That’s the kind of predictable income stream that infrastructure investors are built to underwrite.

UBS noted in its analysis of the FTTH investment landscape that open access structures have become particularly attractive to infrastructure investors because they own the core asset, face minimal concern about competing networks in their territory, and avoid the operational complexity of servicing retail customers directly (source).

The numbers tell the story. Open access fiber entities in Europe have seen enterprise valuations increase substantially — in some cases approaching 10x multiples — while certain vertically integrated telcos have experienced enterprise value contraction over the same period. Wholesale-only fiber models have been cited as generating steady annual returns in the range of 12% to 18%, compared to higher variance outcomes in retail models.

One real-world case from a Scandinavian market illustrates the shift: an electric utility that operated as its own retail ISP for a decade decided to transition to a wholesale open access model. Within three years of the switch, total revenue increased by nearly 40%, staff costs dropped by 25%, and EBITDA margin jumped from 6% to 57%. That’s not a marginal improvement — it’s a fundamental transformation in business economics.

The European Precedent: What Open Access Markets Tell Us

Europe offers the most mature data set for evaluating open access FTTH model performance at scale. Countries with regulated or voluntarily adopted open access frameworks — particularly in Scandinavia, the Netherlands, and parts of Southern Europe — have generally achieved superior infrastructure utilization, faster take-rate ramps, and more competitive pricing for consumers.

Sweden is the standout example. Fiber penetration has grown from roughly 50% to around 95% of households with access to fiber-based broadband, and much of that growth was driven by open access municipal networks where multiple ISPs compete on shared infrastructure.

In markets like Singapore and Italy, where open access fiber plays a prominent role, gigabit-speed packages have become baseline offerings at affordable prices — a direct consequence of the competitive dynamics that open access enables. In markets where a single operator controls both infrastructure and retail, gigabit broadband tends to be positioned as a premium product with significantly higher pricing.

The competitive dynamics differ fundamentally. Open access drives consumer benefit through ISP competition while protecting the infrastructure investor’s revenue — a combination that’s hard to replicate in a vertically integrated model.

Let’s be fair to the retail model. It works well in specific conditions.

If you’re an incumbent with an established consumer brand, deep local market knowledge, and an existing customer base you can migrate onto fiber, retail makes strategic sense. You already have the brand equity, the distribution channels, and the operational infrastructure. Going open access would mean sharing your hard-built competitive advantage with rivals.

Retail also works in markets with limited overbuild risk — dense rural or underserved areas where you’re likely to be the only fiber provider for the foreseeable future. In those contexts, concentration risk is lower because there’s no competing infrastructure to siphon subscribers.

Where retail struggles is in competitive urban and suburban markets where multiple operators are chasing the same homes. The math gets punishing fast: rising build costs, higher cost of capital, and an increasing number of homes served by two or more fiber providers. When your only revenue comes from winning the retail customer, overbuild risk translates directly into stranded CapEx.

Making the Decision: A Framework for Long-Term Value

The open access vs retail decision isn’t about which model is “better” in the abstract. It’s about which model aligns with your capital structure, competitive environment, and long-term strategic ambitions. Here’s a practical framework for thinking through it.

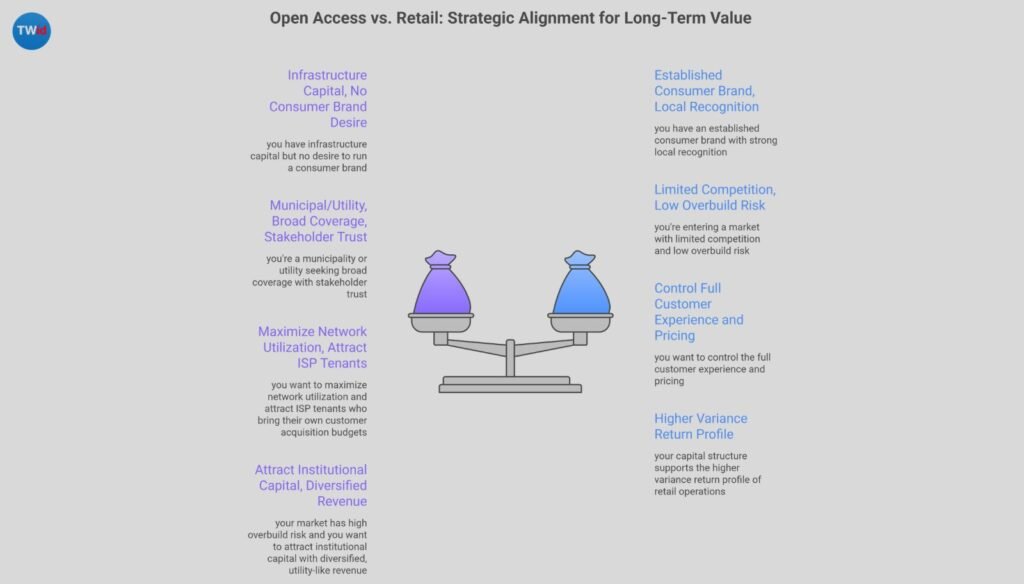

Choose open access if: you have infrastructure capital but no desire to run a consumer brand; you’re a municipality or utility seeking broad coverage with stakeholder trust; your market has high overbuild risk and you want to attract institutional capital with diversified, utility-like revenue; or you want to maximize network utilization and attract ISP tenants who bring their own customer acquisition budgets.

Choose retail if: you have an established consumer brand with strong local recognition; you’re entering a market with limited competition and low overbuild risk; you want to control the full customer experience and pricing; or your capital structure supports the higher variance return profile of retail operations.

Consider hybrid if: you want the control of retail with the upside of wholesale; you can operate as an anchor tenant on your own infrastructure while opening additional capacity to third-party ISPs; or you’re transitioning from a retail model and want to test open access without a full structural shift.

Whatever you choose — commit architecturally from day one. Retrofitting a retail network into an open access platform mid-deployment destroys value and creates operational chaos.

The Bottom Line

The global FTTH market is projected to grow at double-digit rates through the end of the decade. Capital is flowing, competition is intensifying, and the operators who position their networks as high-utilization, investable infrastructure assets will capture disproportionate long-term value.

The open access FTTH model isn’t the right answer for every operator. But the data increasingly suggests it’s the right answer for the market conditions most operators are facing: rising build costs, higher cost of capital, intensifying overbuild, and institutional investors who prefer diversified infrastructure plays over concentrated retail bets.

The question isn’t whether your fiber is good enough. It’s whether your business model is built to extract the maximum value from every strand you’ve deployed.

Start pressure-testing your model against your capital structure, competitive environment, and long-term strategy this quarter. The operators who make this decision with discipline now will be the ones still compounding value a decade from now.

Frequently Asked Questions

What is an open access FTTH model and how does it differ from retail?

An open access FTTH model separates infrastructure ownership from service delivery. A network company builds and maintains the fiber, while multiple ISPs compete to serve customers on the same infrastructure. Retail FTTH bundles everything under one operator — build, operate, and serve. The fundamental difference is who bears the customer acquisition risk and how the network gets monetized.

Why do infrastructure investors prefer the open access FTTH model over retail?

Infrastructure investors favor open access because it produces diversified, contracted revenue streams that resemble utility cash flows. Instead of depending on a single retail brand to win customers, revenue comes from multiple ISP tenants — reducing concentration risk, lowering churn exposure, and creating the kind of predictable income profile that pension funds and infrastructure funds are designed to underwrite.

Can a retail FTTH operator transition to an open access model?

Yes, but it’s expensive and operationally complex if done mid-deployment. The architecture, commercial agreements, and operational workflows are fundamentally different. Operators who anticipate a future move to open access should build with that flexibility in mind from day one — including network design, OSS/BSS infrastructure, and contractual structures. Retrofitting after the fact often destroys more value than it creates.

What take-rates can operators expect under each model?

Single-operator retail networks in competitive urban markets typically achieve take-rates between 30% and 50%. Open access networks with multiple ISPs have reported take-rates ranging from 70% to 90%, because customers are monetized regardless of which retail brand they choose. Higher take-rates translate directly to better infrastructure utilization and faster payback on CapEx.

Is the open access FTTH model only viable in regulated markets?

No. While open access has historically been associated with regulatory mandates in markets like Australia and parts of Europe, an increasing number of operators are adopting it voluntarily as a competitive strategy. In the United States, large telecom companies are exploring joint venture structures that incorporate open access principles — particularly to attract infrastructure capital and reduce overbuild risk in competitive markets.

How AI and FTTH Automation Improve FTTH Network Operations and Fault Management

Every FTTH operator has lived through the 2 AM call. A fiber cut knocks out service to 500 homes. The NOC scrambles. A technician gets dispatched — two hours later — to the wrong location. Meanwhile, churn begins before sunrise.

That reactive loop has been the default operating model for fiber networks since the first strand was lit. But the economics of running networks this way are breaking down fast. Labor costs are climbing. Subscriber expectations for uptime are absolute. And the competitive window between “service restored” and “customer lost” keeps shrinking.

FTTH automation powered by artificial intelligence is changing this equation entirely. Not in theory — in production, right now. According to NVIDIA’s 2026 State of AI in Telecommunications survey, 90% of telecom operators report that AI is already driving positive ROI, and network automation has overtaken customer experience as the leading AI use case for investment.

If you’re running fiber operations without an AI strategy, you’re not just leaving efficiency on the table — you’re falling behind operators who are already using it to predict faults, automate remediation, and cut operational costs by double digits.

Why Traditional FTTH Fault Management Is Failing?

The conventional NOC model was designed for a different era. Operators deploy monitoring tools that generate thousands of alerts daily — most of them noise. Engineers triage manually, correlate symptoms across siloed systems, and escalate based on experience and intuition rather than data-driven prioritization.

The result is painfully predictable. Mean time to repair (MTTR) stretches to hours. Customer-facing outages that could have been prevented become emergency dispatches. And the same fault patterns repeat because root-cause analysis happens after the damage is done — if it happens at all.

For FTTH networks specifically, these problems are amplified by the physical layer. Fiber cuts, splice degradation, optical power drift, and ONT failures all require different diagnostic approaches. A centralized NOC handling hundreds of thousands of subscribers simply cannot process the volume of telemetry data needed to catch issues early.

This is exactly where FTTH automation creates its highest leverage.

How AI Transforms Fiber Network Operations

AI in FTTH network operations is not a single tool — it’s an intelligence layer that sits across your entire operational stack. The most impactful applications fall into three categories: predictive fault detection, automated root-cause analysis, and self-healing network capabilities.

Predictive Fault Detection

The most immediate value of FTTH automation comes from catching failures before they affect subscribers. Machine learning models trained on historical telemetry — optical power levels, error counters, temperature readings, and traffic patterns — can identify the early signatures of degradation days or even weeks before a hard fault occurs.

According to Bain & Company’s research on AI in telecommunications, predictive analytics enables operators to forecast network behavior by analyzing past and real-time data. In practice, this means identifying a weakening splice point or a degrading OLT port before it triggers an outage — and scheduling maintenance during a planned window instead of scrambling at midnight.

The data from cross-industry predictive maintenance implementations is compelling. Research from Deloitte shows that predictive maintenance delivers a 35–45% reduction in downtime and a 70–75% elimination of unexpected breakdowns. For FTTH operators managing tens of thousands of active connections, those percentages translate directly into saved revenue and retained subscribers.

Automated Root-Cause Analysis

When faults do occur, AI dramatically accelerates the diagnostic process. Traditional troubleshooting requires engineers to manually correlate alerts from multiple systems — the optical monitoring platform, the provisioning system, the element management system, the ticketing platform. Each step adds minutes. Minutes add up to hours.

AI-powered root-cause analysis engines ingest data from all of these systems simultaneously. They identify correlations that human operators would miss — for example, recognizing that a cluster of ONT resets in a specific neighborhood coincides with a temperature anomaly on a particular fiber segment, pointing to a splice closure issue rather than individual equipment failure.

NVIDIA’s research highlights that AI-driven platforms can reduce operational costs by up to 40% and shorten fault resolution times by up to 30%. For an FTTH operator running lean NOC teams across a growing footprint, that efficiency gain is the difference between scaling with headcount and scaling with intelligence.

Self-Healing Network Capabilities

The most advanced tier of FTTH automation is the self-healing network — systems that not only detect and diagnose faults but execute remediation automatically, without human intervention.

This doesn’t mean AI is rebooting OLTs on its own without guardrails. The most effective implementations use a tiered trust model. Low-risk actions like restarting a stuck ONT session, clearing an error counter, or rerouting traffic to a backup path execute automatically when confidence levels exceed a set threshold. Higher-impact changes — adjusting optical power levels, reconfiguring VLAN assignments, or modifying QoS policies — are prepared by the AI with full impact analysis but require engineer approval before execution.

Organizations implementing this tiered approach report recovering from common faults in under 60 seconds, compared to 15–45 minutes with manual processes. That’s not a marginal improvement — it’s a structural advantage.

The Business Case for FTTH Automation

If you’re presenting an AI investment to your board, the business case needs to go beyond operational metrics. Here’s how FTTH automation creates value across the business.

Reduced OpEx through NOC efficiency. AI handles the alert triage, correlation, and low-tier remediation that currently consumes 60–70% of NOC staff time. This doesn’t necessarily mean fewer people — it means the same team can manage a significantly larger network footprint without proportional headcount growth.

Lower churn from improved service quality. Every minute of unplanned downtime erodes subscriber trust. Predictive maintenance and faster fault resolution directly reduce the outage events that drive churn. In competitive markets — and as we’ve explored in our analysis of FTTH growth strategies in overbuilt markets — service reliability is one of the few genuine differentiators when price and speed reach parity.

Extended infrastructure lifespan. Continuous monitoring and condition-based maintenance extend the useful life of active equipment. AI identifies components approaching end-of-life based on actual performance data, not arbitrary replacement schedules, optimizing your CapEx cycle.

Faster time to revenue on new deployments. Automated provisioning and AI-assisted network design reduce the time between homes passed and homes connected. For operators racing to monetize their fiber build, this acceleration compounds over every deployment phase.

What FTTH Operators Get Wrong About AI Adoption?

Despite the clear benefits, many fiber operators stumble in their AI implementation. The most common mistakes are worth calling out.

Starting with the wrong use case. Many operators begin their AI journey with customer-facing chatbots or marketing personalization. These deliver value, but the highest-ROI starting point is network operations — specifically, alert correlation and predictive fault detection. The data is already flowing through your monitoring systems. The problem is well-defined. And the impact is directly measurable.

Underinvesting in data quality. AI models are only as good as the telemetry feeding them. Operators running legacy monitoring with 5-minute polling intervals don’t have the data resolution to support meaningful prediction. The prerequisite is streaming telemetry at high resolution — and most operators need to upgrade their data pipeline before they can benefit from ML models.

Treating AI as a vendor product rather than an operational capability. Buying a platform and expecting it to work out of the box is a recipe for expensive shelfware. The operators getting real value from FTTH automation are the ones building internal competency — training their NOC teams to work alongside AI, tuning models to their specific network topology, and iterating on automation playbooks continuously.

For operators still evaluating their broader network strategy — including whether to pursue a retail, wholesale, or open-access model — the AI investment decision should align with your operational model. Open-access operators managing multi-tenant networks, for example, benefit disproportionately from automated SLA monitoring and fault isolation across ISP boundaries.

Where FTTH Automation Is Heading in 2026 and Beyond?

The trajectory is clear. The industry is moving toward telco-specific AI models trained on network data — not generic large language models repurposed for telecom. These purpose-built models understand fiber network topology, recognize fault patterns specific to PON architectures, and reason through diagnostic workflows that reflect actual field conditions.

Digital twin technology is accelerating this shift. Operators are building virtual replicas of their fiber networks that allow AI systems to simulate changes — rerouting traffic, adjusting power budgets, reconfiguring split ratios — before applying them to live infrastructure. This reduces the risk inherent in automation and accelerates the path toward genuinely autonomous network operations.

NVIDIA’s 2026 survey data captures the momentum: 89% of telecom operators plan to increase their AI budgets this year, up from 65% the prior year. Approximately 54% now use AI for network planning, deployment, and optimization — a 17-percentage-point jump from the previous year. Network automation is no longer an experimental initiative. It’s becoming the operational foundation.

For FTTH executives, the strategic question has shifted. It’s no longer “should we invest in AI?” It’s “how quickly can we deploy it, and where do we start?”

Start with your telemetry pipeline. Build observability before intelligence. Deploy anomaly detection before full automation. And move fast — because your competitors already are.

Frequently Asked Questions

1. What is FTTH automation and how does it differ from traditional network management?

FTTH automation uses artificial intelligence and machine learning to monitor, diagnose, and resolve fiber network issues with minimal human intervention. Traditional network management relies on manual alert triage, human-driven diagnostics, and reactive dispatch workflows.

FTTH automation shifts this model from reactive to predictive — identifying faults before they cause outages and executing remediation automatically for low-risk issues. The result is faster resolution times, fewer truck rolls, and significantly lower operational costs.

2. What ROI can FTTH operators expect from AI-driven network operations?

The data is increasingly clear. NVIDIA’s 2026 telecommunications survey found that 90% of operators report positive ROI from AI investments, with network automation identified as the top use case. Cross-industry benchmarks from Deloitte show predictive maintenance reduces downtime by 35–45% and maintenance costs by 25–30%. For a mid-size FTTH operator, this typically translates to measurable OpEx reduction within the first 12–18 months, with compounding returns as models improve with more data.

3. How does predictive maintenance work in fiber optic networks specifically?

Predictive maintenance in FTTH networks relies on continuous monitoring of optical-layer telemetry — including transmit and receive power levels, bit error rates, optical signal-to-noise ratios, and ONT status data.

Machine learning models trained on historical performance baselines detect subtle deviations that indicate degrading splices, failing transceivers, or environmental stress on fiber segments. When the model identifies a high-probability fault precursor, it triggers a proactive maintenance workflow rather than waiting for service-affecting failure.

4. What infrastructure prerequisites do operators need before deploying AI in their NOC?

The most critical prerequisite is high-resolution streaming telemetry. Operators relying on legacy SNMP polling at 5-minute intervals lack the data granularity to support meaningful AI analysis. The shift to model-driven telemetry via gRPC or similar protocols is a foundational investment.

Beyond data infrastructure, operators need a unified data lake that aggregates telemetry from optical monitoring, element management, provisioning, and ticketing systems. AI models deliver the highest value when they can correlate data across these traditionally siloed platforms.

5. Is FTTH automation only relevant for large-scale operators, or can smaller providers benefit too?

Smaller operators often benefit disproportionately from FTTH automation because they’re running leaner NOC teams with less capacity to absorb manual triage workloads. Cloud-based AI platforms have lowered the entry barrier significantly — operators don’t need to build on-premise ML infrastructure to get started.

The key is starting with well-defined, high-impact use cases: automated alert correlation, predictive fiber cut detection, or AI-assisted provisioning. Even a regional operator with 20,000–50,000 subscribers can achieve meaningful ROI from these targeted deployments.

How Open-Access FTTH Networks Improve Utilization and Revenue Yield

If you’re a fiber operator sitting on a half-built network with a take-rate stuck below 35%, you already know the math isn’t working. The CapEx is sunk, the homes are passed, but the revenue is trickling in too slowly to satisfy your investors. What most operators don’t talk about loudly enough is that the business model — not the network — is often the real constraint.

That’s where open-access FTTH economics changes the conversation entirely.

Open-access isn’t just a regulatory compliance play. For operators who structure it correctly, it’s a deliberate strategy to drive higher network utilization, diversify revenue streams, and ultimately improve yield on a capital-intensive asset. This post breaks down how it works, what the data actually shows, and where operators tend to get it wrong.

The Utilization Problem at the Heart of FTTH Economics

Here’s the uncomfortable reality: most fiber networks are built to serve 100% of homes passed but monetized at a fraction of that capacity. The average take-rate in a competitive urban market sits somewhere between 30% and 50%. That means anywhere from half to two-thirds of your deployed fiber is generating zero revenue on any given day.

Traditional vertically integrated operators — those who build, operate, and retail on their own network — carry the full weight of customer acquisition, churn management, and service delivery on top of infrastructure costs. When take-rates lag, every piece of that stack bleeds margin.

The open-access model separates those layers. The network company (NetCo) owns and operates the physical infrastructure. Multiple service providers (ISPs) ride the network and compete for end-users.

The NetCo generates revenue from wholesale access fees, regardless of which ISP wins the customer. This is the structural shift that makes utilization economics genuinely different.

What Open-Access FTTH Economics Actually Means

Before we get into the revenue mechanics, let’s be precise about what we’re talking about. Open-access FTTH economics refers to the financial dynamics created when a fiber infrastructure is opened to multiple competing service providers under a wholesale access model.

The three-layer model looks like this:

Infrastructure Layer: Physical fiber, ducts, passive optical components — owned by the NetCo

Access Layer: Active electronics, network management, SLAs — operated by the NetCo or a neutral operator

Service Layer: ISP retail products, customer billing, marketing — owned by competing service providers

The revenue model for the NetCo is wholesale access fees per subscriber activated, plus potentially dark fiber leases and enterprise connectivity revenues. Because the cost of adding a new tenant onto an existing network is minimal, each additional ISP that joins the platform translates directly to higher margin — incremental revenue without proportional incremental cost.

How Multi-Tenant Networks Drive Higher Utilization

The utilization math shifts substantially when multiple ISPs compete on the same network. Here’s why.

In a single-operator retail model, the operator competes for a customer and either wins or loses. If the customer goes with a competitor on a different network, the operator’s infrastructure sits dark on that home.

In an open-access model, the outcome is different: if a competing ISP acquires that same customer over your network, the NetCo still earns a wholesale fee. The customer is monetized regardless of retail brand preference.

This structural shift transforms the competitive landscape from zero-sum to collaborative at the infrastructure level. More ISPs competing on the network means more customer acquisition activity — funded by the ISPs — which directly drives take-rate on the NetCo’s infrastructure.

UTOPIA Fiber in Utah is the clearest proof point in the U.S. market. The 20-city municipal consortium now hosts 15 competing ISPs across more than 100,000 households and has been operating profitably, with service options ranging from entry-level broadband to multi-gigabit tiers.

The competitive tension between ISPs drove both take-rate growth and pricing competitiveness — without the NetCo absorbing customer acquisition cost.

The European experience makes the same case at scale. Countries with mandated open-access frameworks have consistently achieved higher penetration rates. Spain, with one of the most competitive open-access environments in Europe, has reached a take-up rate above 90% — a figure that vertically integrated operators in less competitive markets struggle to approach.

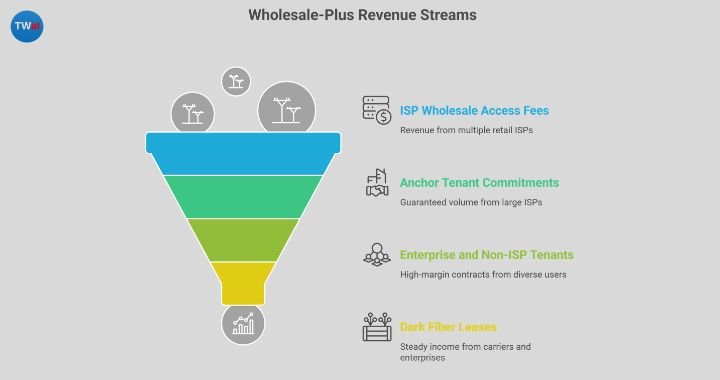

Revenue Yield: The Case for Wholesale-Plus Models

Pure wholesale is one model. But the most financially attractive open-access structures for private operators are what practitioners are calling “wholesale-plus” — where the NetCo earns layered revenues across multiple streams.

Consider what a well-structured open-access network can monetize:

Tier 1 — ISP Wholesale Access Fees Per-subscriber fees from multiple retail ISPs. The more ISPs, the more diversified and resilient this revenue stream becomes. No single ISP departure collapses the revenue base.

Tier 2 — Anchor Tenant Commitments Large ISPs or carriers commit to a minimum take volume in exchange for preferred wholesale terms. This de-risks the early ramp period and supports the initial debt structure. The AT&T and BlackRock GigaPower joint venture uses this logic explicitly — anchor-tenant economics underwrite the build, with additional ISP tenants improving yield over time.

Tier 3 — Enterprise and Non-ISP Tenants Open-access infrastructure can be leased to enterprises, utilities, government agencies, and wireless carriers for backhaul. These are often high-margin, long-duration contracts that are completely uncorrelated to residential broadband churn. Ubiquity, one of the private-sector open-access operators, describes this as making networks “three-dimensional” — multiple uses and multiple providers across the same last-mile infrastructure.

Tier 4 — Dark Fiber Leases Carriers and enterprises willing to manage their own electronics can lease dark fiber strands, providing steady passive income with near-zero operational overhead for the NetCo.

This multi-tier revenue structure is why investor-backed NetCos are increasingly repricing their equity stories to infrastructure-style valuations — CPI-linked fees, long-life cash flows, and diversified revenue bases. It’s also why the model aligns well with growing ARPU strategies. For operators already pursuing ARPU optimization on a retail model, understanding how fiber broadband providers can grow revenue per user without increasing churn becomes directly applicable when transitioning toward wholesale structures.

What the Data Shows About Open-Access Network Performance

The operators who position their networks as neutral infrastructure platforms will attract both ISP tenants and institutional capital more easily than those locked into a single retail brand. Infrastructure capital has a clear preference for diversified, long-duration revenue streams over concentrated retail broadband bets.

The European precedent backs this up at the market level. Countries with regulated open-access frameworks have generally achieved superior utilization, faster take-rate ramp, and stronger competitive pressure that benefits the underlying infrastructure economics.

Sweden’s Stokab (a wholesale-only dark fiber provider in Stockholm) has operated for over two decades as a model of how infrastructure separation creates both investment efficiency and market resilience.

In the U.S., where open-access is not mandated, the adoption is being driven by economics rather than regulation. The current interest rate environment — which pushed minimum FTTH build return requirements from roughly 8–10% in 2021 to 12–15% today — makes the diversified revenue logic of open-access even more compelling for investors who need infrastructure-level certainty.

Where Operators Get the Open-Access Model Wrong

Open-access FTTH economics only work when the execution matches the structure. The most common failure points:

Operational Standardization Is Non-Negotiable The speed at which ISPs can be onboarded — from order to revenue — is one of the defining operational metrics of a NetCo. Without standardized processes and automated provisioning, each new ISP becomes a custom integration project. That kills the scalability that makes the model work.

Anchor Tenant Selection Matters More Than You Think Starting with a weak or uncommitted anchor ISP leaves the NetCo exposed during the ramp period. The best-performing open-access networks enter the market with an anchor-tenant commitment that absorbs a meaningful floor of wholesale fees before the first additional ISP is onboarded.

Pricing Architecture Has to Be Transparent ISPs will only commit to an open-access network if they can model their margins with confidence. Opaque or discretionary wholesale pricing creates distrust and reduces the number of ISPs willing to compete on the platform.

Infrastructure Quality Drives Long-Term Retention The NetCo’s customer is the ISP, not the end-user. But end-user experience is the ISP’s primary SLA requirement. If network reliability, speed consistency, or provisioning quality degrades, ISPs churn off the platform. The infrastructure layer must be operated to enterprise standards.

Is Open-Access the Right Model for Your Network?

Not every fiber network benefits from the open-access structure. The model performs best when:

The serviceable market has competitive DSL or cable infrastructure that multiple ISPs can displace

Sufficient ISP demand exists — or can be cultivated — to populate the wholesale marketplace

The operator is willing to forgo retail brand equity in exchange for infrastructure yield

The capital structure allows for a longer ramp-up before multi-ISP revenues normalize

In markets where only one ISP is likely to ever operate on the network, the open-access structure adds complexity without meaningful revenue benefit. The model pays off when the platform genuinely attracts multiple tenants. That’s what converts underutilized fiber into a revenue-compounding infrastructure asset.

For executives evaluating the transition, the critical question isn’t whether open-access is theoretically superior — the economics generally support it in the right market conditions. The question is whether your current organization, operational stack, and capital structure are positioned to execute it well.

5 Frequently Asked Questions on Open-Access FTTH Economics

1. What is the main revenue difference between an open-access FTTH network and a traditional retail fiber model?

In a traditional retail model, the operator earns revenue only from the customers it directly acquires and retains. In an open-access model, the NetCo earns wholesale fees from every ISP tenant that activates subscribers on the network — regardless of which ISP wins the customer. This diversifies revenue and reduces dependence on any single retail take-rate.

2. Does open-access FTTH always require a regulatory mandate to be viable?

No. While open-access has historically been associated with regulated European markets, private operators and institutional investors in the U.S. are increasingly adopting it for purely economic reasons. The model reduces customer acquisition costs for the NetCo, diversifies revenue, and attracts infrastructure-style capital — independent of any regulatory requirement.

3. How does open-access affect network utilization specifically?

By allowing multiple ISPs to compete for subscribers over the same physical infrastructure, open-access aligns the competitive incentives of ISPs with the NetCo’s utilization goals. More ISPs mean more sales activity, more customer acquisition, and higher overall take-rate — without the NetCo absorbing the retail acquisition cost.

4. What are the biggest risks of transitioning to an open-access or wholesale model?

The primary risks are operational complexity (provisioning multiple ISPs requires standardized systems), anchor tenant dependency (early revenue depends heavily on a committed first ISP), and margin compression in wholesale pricing if the operator underprices access to attract tenants. Getting the wholesale pricing architecture right from the start is critical.

5. What financial metrics should executives track to evaluate open-access network performance?

The key metrics are: wholesale revenue per home passed (not just per subscriber), ISP tenant count and diversity, time-to-revenue per new ISP onboarded, network utilization rate across homes passed, and EBITDA margin by revenue tier. Infrastructure investors specifically focus on revenue durability and diversification — the number of ISP tenants and their combined revenue floor is as important as overall take-rate.

The Bottom Line

Open-access FTTH economics isn’t a theory — it’s a model that’s been stress-tested in some of the world’s most competitive fiber markets and is gaining serious traction with sophisticated capital. The core logic is straightforward: build the infrastructure once, open it to multiple service providers, and earn diversified revenue on every subscriber regardless of which retail brand wins the home.

For FTTH executives navigating a market where build costs are rising, return hurdles are tightening, and competition is intensifying, the utilization and revenue yield advantages of open-access deserve serious strategic consideration.

Ready to evaluate whether an open-access model fits your network and market? Contact us to discuss how the right content strategy can position your organization at the forefront of this shift.

Should an FTTH Operator Choose a Retail, Wholesale, or Open-Access Model?

Choosing the wrong business model for your fiber network is one of the most expensive mistakes an FTTH operator can make — and most teams don’t realize it until they’re already three years into deployment.

In the retail vs wholesale FTTH debate, there’s no universal winner. Each model carries distinct revenue logic, risk exposure, and competitive implications. The right choice depends on your market position, capital structure, and long-term ambitions.

Get it right, and your infrastructure becomes a compounding asset. Get it wrong, and you’re left with stranded assets and a take-rate that won’t cover your WACC.

This post breaks down all three models — retail, wholesale, and open-access — so you can make a strategic decision backed by data, not industry folklore.

The Stakes Are Higher Than You Think

According to the FTTH Council Europe’s 2024 Market Overview, Europe alone passed 280 million homes with fiber — yet household penetration in many markets still sits below 50%. That gap isn’t just a marketing problem. It’s often a structural one: operators chose a business model that limits their ability to monetize the network they built.

Meanwhile, the ITU’s Broadband Commission consistently highlights that open-infrastructure models accelerate adoption in competitive markets. The question is whether those models work for your specific situation.

Let’s dig in.

The Retail FTTH Model: Control, Margin, and Risk

In a retail model, you own the network and serve the end customer directly. You’re the ISP. You handle billing, customer service, marketing, and the whole subscriber relationship.

Why operators choose it

The appeal is obvious: you capture the full revenue stack. No sharing, no margin compression from resellers. You build your brand, own the data, and control the customer experience end-to-end. For markets where you have strong brand equity or first-mover advantage, the retail model is extremely powerful.

Operators like AT&T Fiber in the US and Swisscom in Switzerland have made this work at scale. Their ability to bundle broadband with mobile, TV, and smart home services creates an ARPU story that pure-infrastructure players simply cannot replicate.

Running a retail operation is capital and operationally intensive. You need a customer acquisition engine, a churn management function, a 24/7 support center, and the working capital to fund subscriber growth before you start collecting recurring revenue. In a competitive market — especially one where overbuilders are entering your footprint — margin compression hits hard.

The retail model also concentrates risk. If your take-rate disappoints, there’s no backstop revenue from other ISPs using your network.

The Wholesale FTTH Model: Scale Fast, Share the Revenue

In a wholesale model, you build and operate the passive or active network infrastructure, then lease capacity to one or more retail ISPs. You’re in the infrastructure business, not the subscriber business.

Why it’s gaining traction

The economics are increasingly attractive. You de-risk your revenue by spreading it across multiple service providers. Even if one ISP underperforms, others on your network are still generating traffic and paying access fees. This model is particularly compelling for infrastructure investors — PE firms and pension funds love the predictable, long-duration cash flows.

Countries like the Netherlands have thrived under a quasi-wholesale model. Companies such as Reggefiber (now part of KPN) and independent altnets have demonstrated that institutional capital is far more accessible when the network is positioned as infrastructure rather than a consumer brand.

There’s also a speed advantage. When you’re not building a retail operation in parallel, you can deploy fiber faster. That matters enormously when you’re racing to increase take-rate in homes passed before a competitor locks in the addresses.

The tradeoff

You lose direct customer control and full revenue upside. Your wholesale pricing needs to be competitive enough to attract ISPs but sustainable enough to service your debt and deliver investor returns. Negotiating long-term anchor tenant agreements before you break ground is critical — a wholesale model without committed offtake is a very uncomfortable position.

The Open-Access Model: Maximum Competition, Maximum Coverage

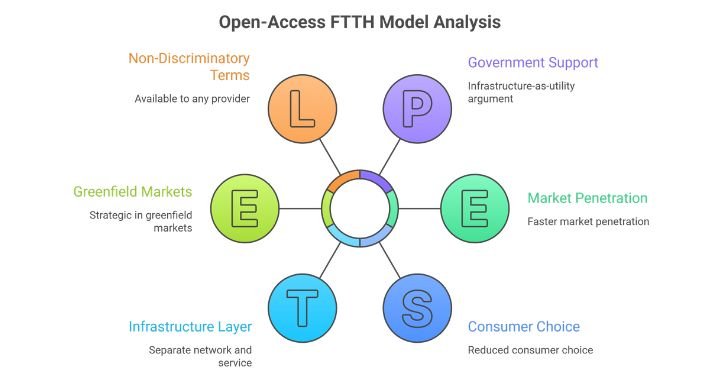

Open access takes the wholesale concept further. Your network is designed from day one to be available to any licensed service provider on non-discriminatory terms. No exclusivity, no preferred partners — open to all.

The infrastructure-as-utility argument

Australia’s NBN Co is the most cited example globally. Built as a government-backed open-access network, it was explicitly designed to prevent incumbent monopoly. The model worked for coverage (nearly universal), though it’s had well-documented challenges with pricing structures and wholesale rate disputes that reduced ISP margins and, in turn, consumer choice.

More refined open-access models are emerging in Sweden, Denmark, and Singapore, where the infrastructure layer is kept strictly separate from the service layer. IDATE DigiWorld research consistently shows that functional or structural separation of network and service layers correlates with faster market penetration in competitive urban areas.

When open access makes sense

If you’re a municipal network, a utility company entering fiber, or a first-time infrastructure investor without a retail brand, open access can be your fastest route to relevance. You’re not trying to win the retail war — you’re trying to make the infrastructure indispensable.

It also works strategically in greenfield markets where no incumbent has footprint. Getting three or four ISPs to commit to your open-access platform before launch creates a far stronger business case for debt financing than a single-ISP retail launch.

Retail vs Wholesale FTTH: Side-by-Side Comparison

Dimension

Retail

Wholesale

Open Access

Revenue ownership

Full stack

Infrastructure only

Infrastructure only

Customer relationship

Direct

Indirect

Indirect

Revenue predictability

Moderate

High (with anchor tenants)

High (diversified)

Capital intensity

Very high

High

High

Time to first revenue

Slower

Faster

Fastest

Brand building

Strong

None

None

Regulatory complexity

Moderate

Low–Moderate

Can be high

Best for

Incumbents, branded altnets

Infrastructure funds, neutral hosts

Municipalities, utilities, greenfield markets

How to Choose: Three Questions Every Executive Should Answer

Rather than defaulting to what competitors do, use these three diagnostic questions to pressure-test your model choice.

1. What is your primary capital constraint? If you’re equity-light and dependent on debt or infrastructure funding, wholesale or open access will typically attract better terms and valuations. Lenders and infrastructure funds price retail customer risk very differently from infrastructure cash flows. If you’re well-capitalized with a consumer brand, retail may generate better long-run equity returns.

2. How competitive is your target market? In markets with two or more existing broadband providers, a retail entry is a fight for market share with high customer acquisition costs. Wholesale or open access positions you above the competitive fray. In underserved or rural markets with no incumbent fiber, retail can be highly profitable with limited competition.

3. What’s your 10-year exit or evolution strategy? Infrastructure-only models tend to attract strategic acquirers and institutional capital at higher multiples. Retail ISPs are valued differently — on EBITDA and churn metrics rather than asset value. If an infrastructure sale or IPO is in the plan, your business model architecture matters enormously for valuation.

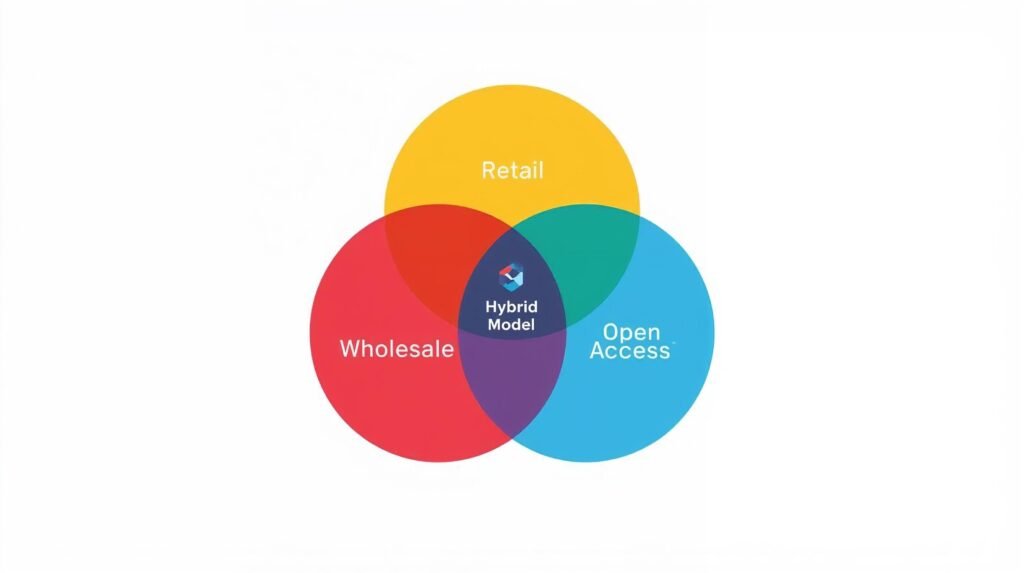

Hybrid Models: The Best of Both Worlds (With Caveats)

Many operators are increasingly running hybrid approaches — owning the passive network and offering it on wholesale terms while also operating a retail brand. This isn’t new (BT Openreach in the UK is the most famous example), but the operational complexity is real. You need genuine Chinese walls between your retail and wholesale teams, or your wholesale partners will not trust the arrangement.

Done well, hybrids maximize revenue and preserve competitive optionality. Done poorly, they create regulatory exposure and destroy wholesale relationships.

Frequently Asked Questions

1. What is the difference between a wholesale and an open-access FTTH model?

In a wholesale model, the infrastructure owner selects and contracts with one or a few retail ISPs to use the network. There may be exclusivity or preferred pricing arrangements. In an open-access model, the network is available to any licensed service provider on equal, non-discriminatory terms — no exclusivity allowed. Open access is essentially wholesale with a stricter neutrality requirement.

2. Which FTTH business model generates the highest ARPU?

The retail model typically generates the highest ARPU per subscriber because the operator captures the full service revenue — broadband, TV, mobile bundles, and value-added services. However, wholesale and open-access models can generate competitive returns on invested capital (ROIC) because their cost structures are leaner and their revenue is more predictable.

3. Can a small altnet viably run a retail FTTH model?

Yes, but it’s operationally demanding. Small altnets that succeed in retail typically focus on a tight geographic footprint, differentiate on service quality rather than price, and keep overhead lean. Many eventually shift toward a wholesale or hybrid model as they scale, because the economics become more attractive for capital recycling and exit optionality.

4. How does the choice of FTTH business model affect access to infrastructure financing?

Infrastructure funds and pension capital strongly prefer wholesale or open-access models because the revenue profile resembles utility cash flows — long-term, contracted, and not dependent on consumer churn dynamics. Retail FTTH operators typically access financing through different channels: bank debt, strategic equity, or operator-backed capital. The model choice directly shapes your investor universe.

5. Is the open-access model always regulated, or can it be voluntary?

Open-access can be either. In some markets (Australia’s NBN, Sweden’s municipal networks), it’s mandated by regulation or government policy. In others, operators voluntarily adopt open access as a competitive strategy — to attract ISP partners, access public subsidy programs, or differentiate from vertically integrated incumbents. Voluntary open access is growing in markets where neutral host positioning creates a genuine commercial advantage.

The Bottom Line

The retail vs wholesale FTTH decision is ultimately a bet on where you create the most value — at the infrastructure layer or the service layer. Both can generate excellent returns. Both carry real risks. The operators who struggle are those who pick a model without fully pressure-testing it against their capital structure, competitive environment, and long-term strategy.

Be honest about your strengths. If you have a consumer brand, go retail and defend it aggressively. If you have infrastructure capital and no desire to run a call center, build the best wholesale platform in your market. If you’re a municipality or utility, open access may be the fastest path to ubiquitous coverage and stakeholder trust.

Whatever you choose — commit to it architecturally from day one. Retrofitting a retail network into an open-access platform mid-deployment is one of the most expensive lessons in fiber infrastructure.

Ready to sharpen your FTTH content and thought leadership strategy? Explore how professional FTTH ghostwriting can help you turn complex operational insight into compelling executive content that opens doors.

8 Ways FTTH Operators Can Increase Take-Rate in Homes Passed

Homes Passed is a deployment milestone. It is not a growth strategy.

For FTTH operators, the real commercial test begins after the network is live: converting homes passed into active, revenue-generating subscribers at a rate that supports payback, margin, and long-term network expansion.

That is where many operators encounter a performance gap. The footprint is in place, the addressable base is real, and service is technically available, yet subscriber uptake lags expectations. In most cases, the problem is not coverage. It is a conversion.

Low take-rate in already homes passed typically reflects a mix of commercial, operational, and go-to-market issues. Households may not know that fiber internet is available. They may not see enough economic or service value to switch. They may begin the purchase journey and drop out because the digital path or installation process introduces too much friction.

For operators, this is one of the highest-leverage opportunities in the business. Increasing take-rate within the existing footprint usually delivers a better near-term return than pursuing incremental build in new areas. It improves capital efficiency, strengthens the business case for future deployment, and drives better monetization from infrastructure that has already been funded and built.

This article outlines why homes passed fail to convert and how FTTH operators can systematically improve take-rate through better segmentation, sharper positioning, cleaner offer design, stronger conversion paths, and tighter install execution.

What take-rate mean in FTTH

In FTTH, the take-rate is the percentage of homes passed by the network that become active subscribers.

If an operator passes 20,000 homes and 7,000 subscribe, the take-rate is 35%.

From an operator standpoint, take-rate is not just a commercial KPI. It is a core measure of network monetization. Homes passed indicate reach. Take-rate indicates whether that reach is translating into cash flow, customer base growth, and a viable return on invested capital.

This distinction matters. Network build metrics can create the appearance of momentum, but they do not by themselves improve unit economics. A stronger take-rate does. It raises revenue density within the footprint, improves capital productivity, and can materially shorten payback periods at the cohort or market level.

For that reason, operators looking to improve growth performance should treat take-rate improvement in already homes passed as a strategic priority rather than a secondary sales metric.

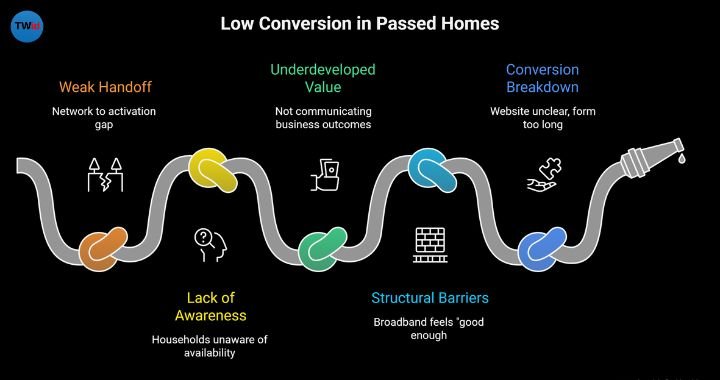

Why already homes passed still not convert

Most low-conversion footprints do not suffer from a single problem. They suffer from a weak handoff between network availability and customer activation.

In some markets, the issue is awareness. Fiber is available, but the household either does not know it or does not fully understand that service is available at their exact address. In others, awareness exists, but the value proposition is underdeveloped. The operator communicates speed, but not business outcomes or everyday customer relevance.

There are also structural barriers to switching. Households may already have broadband that feels “good enough.” Without a clear trigger, price advantage, service differentiation, or trust signal, inertia wins. This is especially true in markets where incumbents have strong brand familiarity or where operators rely on generic messaging such as “faster internet” without making the operational superiority of fiber tangible.

Conversion often breaks down even later in the funnel. The address is serviceable, the lead is interested, and the order journey begins, but the website is unclear, the form is too long, or installation introduces delay and uncertainty. In those cases, demand exists, but the operator fails to capture it.

The result is a monetization shortfall inside a footprint that should be producing more value.

How FTTH operators can increase take-rate in already passed homes

1. Move from footprint-wide marketing to micro-market prioritization

One of the most common commercial mistakes in FTTH is treating all homes passed as equally convertible.

They are not.

Conversion propensity varies significantly by neighborhood, housing type, competitive dynamics, household profile, previous campaign response, service pain points, and even local word-of-mouth. Operators that market uniformly across the entire footprint often dilute budget and message precision.

Identify the pockets with the highest probability of conversion and allocate acquisition resources accordingly. That may include neighborhoods with weak incumbent satisfaction, strong upload-related use cases, recent move-in activity, high remote-work concentration, or stronger historical response to fiber availability campaigns.

This improves more than efficiency. It creates a better operating model for learning. Instead of asking which general campaign worked, operators can measure which combination of segment, message, offer, and channel produced the strongest lift in a specific cluster and then scale that logic across the footprint.

2. Position fiber internet around customer outcomes, not network terminology

Operators understand the technical value of fiber. Most households do not buy on technical architecture.

They buy on outcomes.

That means the commercial message should begin with confirmed availability and quickly translate that availability into practical value: higher reliability, better upload performance, smoother streaming, stronger work-from-home performance, and less service degradation under multi-device usage.

Too many FTTH campaigns still sound like product sheets.

They emphasize infrastructure language that may be accurate but does little to change behavior. Stronger-performing operators frame the offer around why switching improves the customer’s daily experience and why it is worth making the move now.

In commercial terms, this is a positioning issue. If the message does not create a meaningful perception gap between fiber and current service, the take-rate will remain below potential even in fully passed areas.

3. Simplify plan architecture and reduce decision friction

A passed home does not need more options. It needs a clear reason to convert.

Complex plan structures, layered promotional language, installation disclaimers, and too many speed-tier decisions can reduce response rates even when the product is highly competitive. Every extra decision introduces delay and increases the chance that the prospect defers action.

Operators generally perform better when they streamline plan presentation and lead with one clearly positioned hero offer. That offer should make three things immediately obvious: what the customer gets, what it costs, and what is required to get started.

This does not mean sacrificing segmentation or ARPU strategy. It means reducing early-stage friction in the acquisition funnel. Once the household is engaged, upsell logic and packaging flexibility can still play a role. But at the point of conversion, simplicity is often a commercial advantage.

4. Treat installation as a conversion lever, not a downstream function

Operators often think about installation as a service delivery issue. In reality, it is also a sales issue.

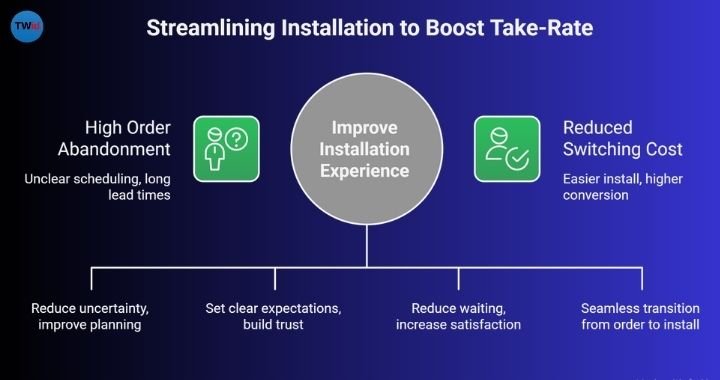

A household that submits an order but faces unclear scheduling, long lead times, poor communication, or multiple reschedules is still at risk of non-conversion. In many footprints, the gap between order intent and service activation is where take-rate underperforms.

Operators that improve take-rate tend to reduce friction between order and install. That includes tighter appointment windows, better pre-install communication, clearer customer expectations, faster activation timelines, and stronger coordination between sales and field operations.

The operational logic is straightforward: the easier the install experience feels, the lower the perceived switching cost. When switching cost drops, conversion tends to rise.

This is especially important in competitive markets where the incumbent can retain a customer simply because changing providers looks inconvenient.

5. Build local proof and neighborhood credibility

Fiber adoption is often hyperlocal. Trust is built at the neighborhood level before it scales at the market level.

For already passed homes, that makes local proof a significant commercial asset. Households are more likely to convert when the service feels established nearby, not merely available in theory. Testimonials, neighborhood-specific case studies, local signage, community references, and “now live on your street” messaging all help reduce perceived risk.

This is not just branding. It directly affects conversion behavior. In many cases, households hesitate not because they object to fiber internet, but because they do not yet feel confident enough to switch from a known provider. Local validation shortens that trust gap.

Operators that succeed here create a sense of momentum within the footprint. The offer becomes less about a new utility choice and more about an upgrade already being adopted by nearby households.

6. Align acquisition efforts with switch-ready moments

Demand for fiber internet is not evenly distributed across time.

Households become more receptive to switching during specific moments: a move, a lease renewal, back-to-school, a work-from-home change, a service outage with the incumbent, or a billing increase from the current provider. Operators that identify and act on these triggers typically see stronger conversion than those running static messaging year-round.

This is where lifecycle thinking becomes important. Homes Passed should not be treated as a one-time launch audience. They should be managed as an addressable conversion base with varying readiness states.

An operator that tracks and re-engages prior non-converters, availability-check users, abandoned orders, and recently homes passed can create much more relevant outreach sequences. That increases acquisition efficiency and often improves take-rate without meaningfully increasing market-level spend.

7. Improve the digital path from availability check to order

In many FTTH footprints, digital execution is an overlooked bottleneck.

The address checker is slow. The availability message is ambiguous. The landing page introduces too much copy before confirming relevance. The form requests too much information upfront. The call to action is weak. Each of these points increases drop-off.

From an operator perspective, this is a conversion-rate optimization problem. Once a household is aware that fiber is available, the path to order needs to be fast, credible, and low-friction. The core digital journey should confirm serviceability, communicate value quickly, show straightforward pricing, and move the prospect toward order completion with minimal distraction.

Mobile performance matters as well. A meaningful share of availability searches and initial consideration happens on mobile devices. If that experience is poor, the funnel will underperform even when upstream marketing is effective.

8. Continue marketing to non-converted passed homes

Low initial response should not be interpreted as zero demand.

Many operators underinvest after the launch window. They send one or two awareness pushes, measure early take-rate, and then shift focus elsewhere. That leaves a large amount of value in the existing footprint.

Homes passed that did not convert on first exposure remain highly relevant prospects. They may have had no immediate trigger, they may have lacked confidence in switching, or they may simply have needed a better message, offer, or reminder. Follow-up through direct mail, retargeting, email, field sales, or localized digital campaigns can materially improve cumulative take-rate over time.

From a unit-economics standpoint, this is attractive. The network is already in place. The address is known. The main challenge is conversion timing and execution.

Operators that treat passed-home acquisition as an ongoing program rather than a launch event generally extract more value from the same footprint.

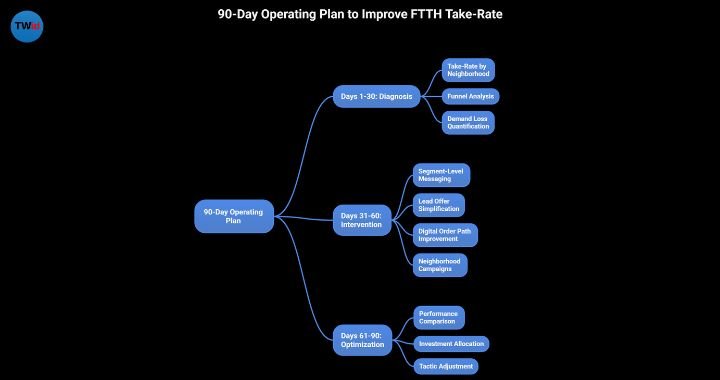

A 90-day operating plan to improve take-rate

For operators looking to improve performance quickly, a structured 90-day approach is often more effective than broad transformation language.

In the first 30 days, the objective is diagnosis. Analyze take-rate by neighborhood, identify the highest and lowest converting segments, review the funnel from awareness to install, and quantify where demand is being lost. This includes digital drop-off, order abandonment, install delays, and segment-specific underperformance.

In days 31 through 60, operators should activate targeted interventions. Refine segment-level messaging, simplify the lead offer, improve the digital order path, and address major installation pain points. At the same time, launch neighborhood-based campaigns where conversion lift is most likely.

In days 61 through 90, the focus should shift to optimization and scale. Compare performance by message, offer, geography, and channel. Increase investment behind the highest-converting plays. Pull back from tactics that are not producing movement in take-rate or downstream activation metrics.

This type of program creates operational discipline around what is otherwise often treated as a marketing problem alone.

The KPIs operators should track

To improve take-rate, operators need to measure more than coverage and gross adds.

The relevant KPI set should include take-rate by cluster, availability-check-to-order conversion, order-to-install completion rate, install lead time, channel-level acquisition cost, cohort-level payback signals, and early churn.