FTTH Overbuild Strategy — And the Five Moves That Win

Most fiber executives facing a second competitor in their market make the same three moves: sharpen the pricing pencil, launch a brand campaign, and announce a new speed tier. Within eighteen months, margins are compressed, churn is roughly unchanged, and the competitor is still there.

Overbuilding is not a temporary disruption that resolves itself. It is the permanent competitive state of any mature fiber market — and the strategies built for greenfield expansion do not work once a second fiber strand runs down your street.

FTTH growth strategies in overbuilt markets require a fundamentally different playbook, and the operators learning that lesson late are already paying for it.

The Overbuild Reality Check

The numbers have moved fast. In 2022, roughly 4% of U.S. homes had access to two or more FTTH providers. By the end of 2023, that figure had nearly doubled to 7.2%. With fiber now passing over 98 million U.S. homes and 84% of potential secondary and tertiary passings still untapped, the competitive pressure has only one direction to go.

The math is compounding. Nearly 60% of remaining attractive build opportunity sits in markets with over 50% existing fiber coverage — meaning new entrants are increasingly chasing adjacencies to already-served territory, not whitespace. Build costs have risen approximately 6% annually. Return minimums have climbed from 8–10% in 2021 to 12–15% today. The operators who can still make the economics work are those with the structural advantages to justify the risk — not those hoping the second fiber provider will eventually retreat.

Here is the reframe that matters: overbuild is not a price problem or a marketing problem. It is a business model problem. The operators who treat it as the former will fight the wrong battle. Those who treat it as the latter will use the pressure to build something their competitor cannot easily replicate.

Why the Standard Overbuild Playbook Fails

Before examining what works, it is worth being direct about what does not — because the conventional responses are not just ineffective, they actively accelerate the margin erosion they are meant to prevent.

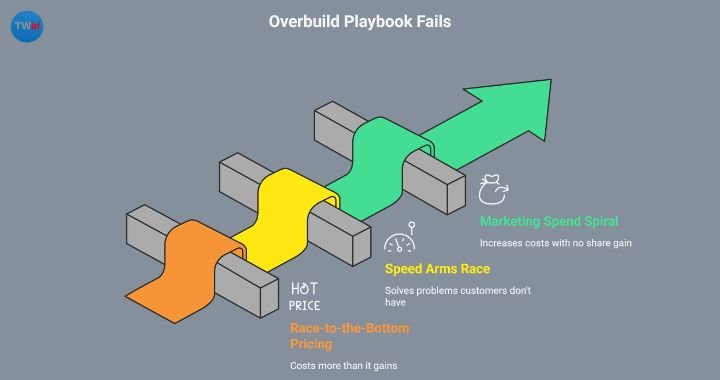

The Race-to-the-Bottom Pricing Trap

The instinct to drop prices when a competitor enters is understandable. It is also wrong in most cases.

A 15% price reduction in a market with a 45% take rate and a $65 ARPU does not win back meaningful share — it simply costs you $9.75 per month on every customer you already have. The subscribers most likely to switch for price alone are also the subscribers with the lowest lifetime value and the highest propensity to churn again when the next promotion appears. You are competing for the wrong customers at the worst possible unit economics.

Price wars have a predictable winner: the operator with the deeper balance sheet. In a market where a well-capitalized overbuilder is entering, the incumbent rarely holds that advantage. The correct response is to make price a less decisive factor — not to race toward the floor.

The Speed Arms Race Nobody Asked For

Gigabit is now table stakes. Symmetrical 10Gbps is a compelling engineering achievement. It is not a customer acquisition strategy.

Residential broadband usage patterns have not changed in ways that make symmetrical multi-gig service a meaningful differentiator for the overwhelming majority of households. Bandwidth demand is growing at roughly 20% annually, driven by streaming, remote work, and smart home devices — applications that are well served by today’s gigabit tiers. Investing heavily in speed differentiation solves a problem your customers do not have, while leaving unaddressed the problems they actually do have: installation friction, service reliability, and support quality.

Technical differentiation in residential fiber is largely illusory. Both operators have fiber. Both have low latency. Competing on a dimension where the gap is invisible to the customer is not a strategy — it is a capital misallocation.

The Marketing Spend Spiral

The reflex to increase brand spend when a competitor enters is understandable and nearly always counterproductive. Marketing can accelerate a structural advantage. It cannot manufacture one that does not exist.

In overbuilt markets, both operators typically increase customer acquisition spend simultaneously. The result is symmetric cost inflation with no net share gain — CAC rises for both, conversion rates fall for both, and the only winners are media buyers. The root problem is structural, not perceptual. No campaign budget resolves a situation where two identical-looking services compete on identical terrain.

The Five FTTH Strategies That Actually Work

The operators growing in overbuilt markets share a common characteristic: they stopped competing on the dimensions where competition is most intense and started winning on dimensions their competitor had not prioritized.

1. Win the Vertical Segments Your Competitor Ignores

Mass-market residential broadband is where the overbuild battle is loudest and margins are thinnest. It is also where your competitor is most focused. The structural opportunity lies in the segments they are ignoring.

Small and medium businesses in fiber-served markets are chronically underserved by residential-grade products but underserved by enterprise pricing and complexity. Multi-dwelling units represent density that dramatically improves per-passing economics, but most overbuilders approach MDU relationships as an afterthought. Anchor institutions — schools, healthcare facilities, municipal buildings — provide long-term contracted revenue that is structurally immune to consumer churn dynamics.

The strategic exercise is identifying the two or three verticals where your network architecture provides a genuine structural advantage over the competitor — whether that is existing conduit access, existing MDU relationships, or technical capability in enterprise-grade service delivery. Pricing power lives in specialization. A fiber provider that owns the SMB segment in a market commands ARPU that mass-market competition cannot touch.

2. Turn Churn Defense Into a Revenue Strategy

Retention spending is typically treated as a cost center. In overbuilt markets, it is the highest-ROI activity available.

The operators growing ARPU in competitive markets are not doing so through new subscriber acquisition — they are doing so through proactive upgrade programs that move existing customers up the value stack before a competitor’s promotional offer becomes the trigger for defection. A customer on a managed Wi-Fi package with a proactive monitoring service is not the same customer as a subscriber on a basic gigabit plan, regardless of how similar the underlying infrastructure is.

The metric that should anchor your competitive analysis is not take rate — it is monthly revenue per passing. Take rate tells you how many homes you are serving. Revenue per passing tells you how much value you are extracting from the market, regardless of what the competitor is doing with the other homes. Operators who optimize for this metric consistently outperform those optimizing for subscriber count.

The practical implication: every retained customer is an upgrade opportunity. Build a retention motion that leads with value addition before the churn signal appears.

3. Weaponize Your Install and Service Experience

In a two-fiber market, the activation experience is often the deciding factor — not because customers research it in advance, but because first-mover advantage in a household compounds over years. The operator who completes a frictionless installation first, with professional equipment placement and a working managed Wi-Fi setup, creates inertia that a competitor’s promotion must overcome.

Service quality as a competitive moat is not theoretical. It is measurable. A 20-point NPS gap between two fiber providers in the same market translates into meaningfully different churn rates, meaningfully different word-of-mouth acquisition, and meaningfully different win rates when the competitor’s promotional pricing expires.

The specific elements that matter: installation scheduling reliability (not just speed), proactive outage communication before the customer notices an issue, and enterprise-grade support tiers for the business customer segments described above. These are operational investments that do not show up in a speed test but determine whether a customer stays for two years or ten.

4. Restructure Partnerships Before Your Competitor Does

The most durable competitive positions in overbuilt markets are not won through customer acquisition — they are won through structural agreements that make competitive entry more difficult or less attractive.

MDU access agreements with exclusivity provisions, long-term municipal right-of-way arrangements, and anchor tenant contracts that provide revenue floor certainty are all assets that reduce competitive exposure at the network level rather than the customer level. An overbuilder calculating the ROI of entering a market does that math on available homes. A market where 30% of MDU density is locked into long-term agreements with an existing operator looks materially different than one without those agreements.

Long-term wholesale arrangements serve a similar function. A competitor that can access your network on commercial terms to serve their own retail customers has less financial incentive to build parallel infrastructure. Network utilization floors protect your economics regardless of what happens at the retail level.

The partnership conversation is time-sensitive. These agreements are far easier to structure before a competitor arrives than after. The operator who moves first on MDU relationships, municipal agreements, and wholesale terms owns the structural advantage for years.

5. Use M&A and Network Sharing to Change the Competitive Math

In mature overbuilt markets, consolidation is not a risk to be managed — it is the likely outcome. The question is whether you position yourself as the consolidator or the consolidated.

Network sharing agreements — both active (sharing active equipment) and passive (sharing conduit, poles, and duct) — offer a path to margin recovery that does not depend on subscriber growth. Two operators running parallel fiber builds through the same geography is economically inefficient for both. Passive infrastructure sharing reduces per-unit build costs and can restore project-level economics that rising interest rates and build cost inflation have made marginal.

The M&A decision framework is portfolio-based, not market-by-market. In markets where you have structural advantages — strong MDU penetration, institutional relationships, low churn — the right answer is often to acquire the overbuilder rather than compete indefinitely. In markets where the competitive position is weak and structural improvement is unlikely, an orderly exit at a reasonable valuation is preferable to years of margin compression followed by a distressed exit.

The operators who will be in the strongest positions in 2028 are the ones making these portfolio decisions now, while optionality is still available.

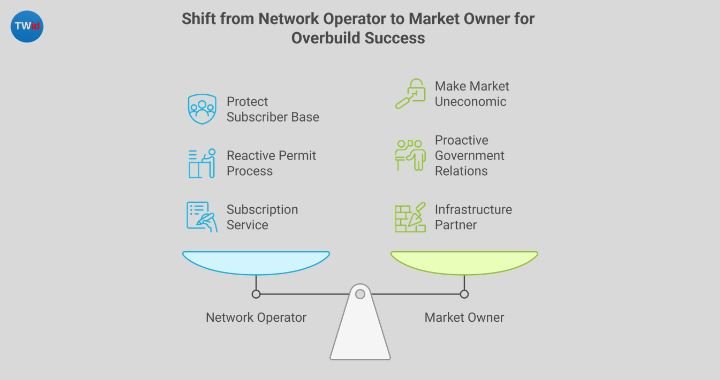

The Mindset Shift: From Network Operator to Market Owner

Every strategy above has a common thread: it is easier to execute if you think of yourself as owning a market rather than operating a network in one.

A network operator’s competitive frame is: how do we protect our subscriber base? A market owner’s competitive frame is: what would it take for this market to be structurally uneconomic for a second fiber provider?

Market ownership looks different operationally. It means building relationships with local government before you need permits, not when you do. It means being the fiber provider that economic development officials call when businesses are evaluating location decisions. It means being visible in community institutions in ways that make your brand synonymous with the market’s connectivity future — not just another ISP.

This positioning is not marketing spend. It is relationship capital built over years of showing up as a community infrastructure partner rather than a subscription service. And it is nearly impossible for a competitor to replicate quickly, regardless of how much they are willing to spend on customer acquisition.

Building FTTH Overbuild Strategy Playbook

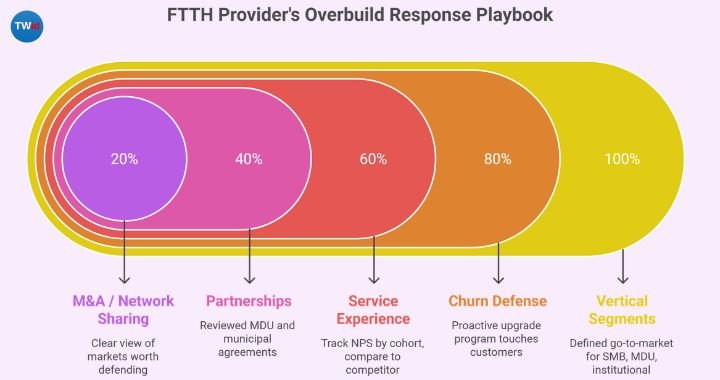

The five strategies above are not sequential — they are simultaneous. But the practical starting point is an honest audit of your current position across each dimension.

For each strategy, answer one diagnostic question:

- Vertical segments: Do you have a defined go-to-market for SMB, MDU, or institutional customers that is separate from your residential motion — with dedicated pricing, products, and sales capacity?

- Churn defense: Do you have a proactive upgrade program that touches customers before a competitor does, or is your retention motion reactive?

- Service experience: Do you track NPS by cohort, and do you know how your score compares to the competitor’s?

- Partnerships: Have you reviewed your MDU and municipal agreements in the past twelve months, and do you know which relationships are at risk of competitor approaches?

- M&A / network sharing: Does your leadership team have a clear view of which markets in your portfolio are worth defending, and which would be better consolidated or exited?

If you cannot answer these questions with specificity, that is the starting point. A 90-day sprint to assess, decide, and assign ownership across these five dimensions costs almost nothing compared to the alternative: competing on price and speed until the economics force a decision that is no longer yours to make.

The one question every FTTH executive should be able to answer before a competitor arrives in their market: “Why would a customer choose us if price were identical?”

If the honest answer is “they wouldn’t,” the work starts now.

FAQ: What FTTH Executives Are Asking Right Now

Does BEAD funding make overbuild worse or better for established operators?

For established urban and dense suburban operators, BEAD is largely separate from the competitive dynamics you are managing today. BEAD targets underserved and unserved areas — the overbuild risk is concentrated in dense suburban adjacencies where multiple operators are chasing the same remaining attractive build opportunity, not in BEAD-eligible rural markets.

Where BEAD does affect established operators is on the supply chain side. BEAD construction timelines converging with AI data center fiber demand in 2026 is creating real fiber supply constraints. Operators planning major builds should be securing supply contracts now rather than assuming availability on standard lead times.

Our take rates are around 40–45%. Is that acceptable in a competitive market?

Industry data from the Fiber Broadband Association’s December 2025 survey puts average primary market take rates at 46.5%. Interestingly, in markets where a secondary fiber provider enters, combined take rates typically rise to approximately 61% — suggesting that competition expands the addressable subscriber pool rather than simply dividing an existing one.

The more important metric is monthly revenue per passing, not raw take rate. A 40% take rate with strong SMB penetration and managed services ARPU can be significantly more valuable than a 55% take rate on commodity residential broadband. Do not optimize for the metric that looks best; optimize for the one that drives long-term business value.

How does the AI and data center boom affect our FTTH strategy?

Two ways, and they are both significant. First, AI infrastructure is competing with FTTH for the same fiber supply. Corning has reported 58% year-over-year enterprise sales growth driven by AI network demand, and AI-focused data centers require dramatically more fiber per rack than traditional infrastructure.

Operators planning capital programs should factor supply constraints and rising costs into their build schedules.

Second, the AI boom is driving demand for high-capacity enterprise-edge connectivity — a direct revenue opportunity for FTTH operators with the right network architecture and enterprise go-to-market capability.

The businesses that need AI-capable connectivity are often in the same markets as your existing residential network. This is a meaningful ARPU expansion opportunity if you build the product and sales motion to capture it.

Should we be considering open-access network models to survive overbuild?

Open-access is gaining real traction in the U.S. after demonstrating its viability in Europe, and it is worth serious evaluation — but it is not a universal answer. The model makes the most sense for operators who want to maximize infrastructure utilization and reduce risk by monetizing the network layer, accepting lower retail margins in exchange for higher network-level returns and reduced churn exposure.

The trade-off is retail margin and customer relationship control. If your competitive strategy depends on owning the customer experience — managed services, enterprise relationships, community positioning — open access may undermine the differentiation you are trying to build. The decision should follow your strategic positioning, not precede it.

With build costs up ~6% annually and return minimums now at 12–15%, when does a new build stop making sense?

The economics have tightened materially since 2021, when the same return minimums sat at 8–10%. The restoration of 100% bonus depreciation in federal tax law for 2026 provides a meaningful one-time capex offset — analysts estimate this could fuel a 5–15% increase in FTTH capex spending — but it does not structurally change the underlying project economics.

The practical decision rule: build only where you can credibly own the market long-term. A new build into a market where you will be the second fiber provider requires a clear answer to why you will win the structural position over time, not just whether the initial take rate assumptions pencil out.

If you cannot articulate a path to market ownership, the capital is better deployed defending and expanding the markets where you already have structural advantages.

Is fixed wireless access (FWA) a real competitive threat to FTTH in overbuilt markets?

Yes, in specific segments — and underestimating it is a mistake. FWA competes most effectively in the 100–300 Mbps residential tier at aggressive promotional price points, which is precisely the tier being commoditized in overbuilt fiber markets.

For price-sensitive subscribers who do not require symmetrical speeds, multi-device density, or the latency performance that fiber delivers, FWA is a credible alternative.

The structural answer remains fiber’s advantage on latency, symmetry, reliability, and capacity for households with five or more connected devices.

FWA is a real threat in the price-sensitive residential segment, not in enterprise, MDU, or high-usage residential — which is another argument for moving your mix toward the segments where FWA cannot credibly compete.

Conclusion: Overbuild Is a Filter, Not a Ceiling

The FTTH markets that will matter in 2028 and 2030 are being shaped by decisions made today — before consolidation forces the issue, before partner agreements are locked up by competitors, and before the operators with the weakest strategic positions have exhausted their options.

Overbuilt markets do not eliminate growth. They filter for operators with the business model discipline, structural positioning, and strategic clarity to earn it.

The playbook above is not about surviving overbuild. It is about using the pressure to build something more durable than what existed before the competitor arrived.

Audit your position across the five strategies this quarter. Identify the one where the gap is largest and the opportunity is most immediate. Start there.

The market will consolidate around the operators who moved first. Make sure you are one of them.