Open Access FTTH Model vs Retail FTTH: Which Business Model Creates More Long-Term Value?

Most fiber executives don’t get to choose their business model twice. Once you’ve committed billions in CapEx to a retail or open access FTTH model, unwinding that decision mid-deployment is one of the most expensive mistakes in the industry.

And yet, the choice between open access and retail FTTH is often made too early, too quickly, and without enough financial modeling behind it. The result? Stranded assets, underwhelming take-rates, and a network that never reaches the utilization levels needed to justify its cost of capital.

This post breaks down both models — not from a textbook perspective, but from the standpoint of long-term value creation. We’ll look at what the data actually says about revenue yield, investor sentiment, and competitive resilience so you can make a strategic decision that compounds over the next two decades.

Understanding the Two Models: Structure Shapes Everything

Before comparing outcomes, it’s worth being precise about what we’re comparing.

Retail FTTH is the vertically integrated model. The operator builds the fiber infrastructure, manages the network, and sells broadband services directly to end customers. Everything — from CapEx to customer service calls — sits on one balance sheet. Revenue comes from monthly subscriptions, and the operator competes for customers against every other provider in the market.

Open access FTTH separates infrastructure from service delivery. A network company (often called a NetCo) builds and operates the fiber plant, then opens it to multiple internet service providers who compete on that same network. Revenue for the NetCo comes from wholesale access fees per activated subscriber, potentially supplemented by dark fiber leases and enterprise connectivity.

The structural distinction is simple. The financial consequences are not.

If you’re weighing the merits of retail, wholesale, and open access models in more detail, this breakdown of how each FTTH business model shapes competitive strategy is a useful starting point before diving into valuation math.

The Open Access FTTH Model: Where the Utilization Math Shifts

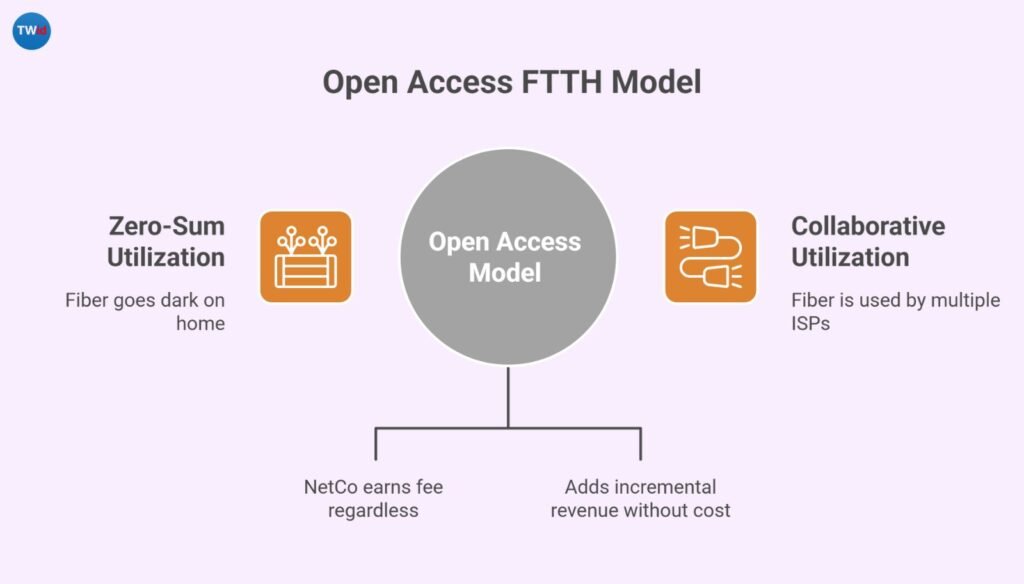

Here’s the core economic argument for the open access FTTH model: it changes the utilization equation from zero-sum to collaborative at the infrastructure level.

In a retail model, if a customer picks a competitor on a different network, your fiber goes dark on that home. You either win the subscriber or earn nothing. In an open access model, the customer might choose a different ISP — but they’re still running over your fiber. The NetCo earns a wholesale fee regardless of which retail brand the customer prefers.

The take-rate implications are significant. Open access networks with multiple ISPs have reported take-rates as high as 70% to 90%, compared to the 30% to 50% range that’s typical for single-provider networks in competitive urban markets. That gap matters enormously when you’re trying to generate returns on capital-intensive infrastructure.

Each additional ISP on the platform adds incremental revenue without proportional incremental cost. The marginal economics are compelling — which is exactly why institutional investors have started paying attention.

The Retail Model: Higher Margins Per Subscriber, Higher Concentration Risk

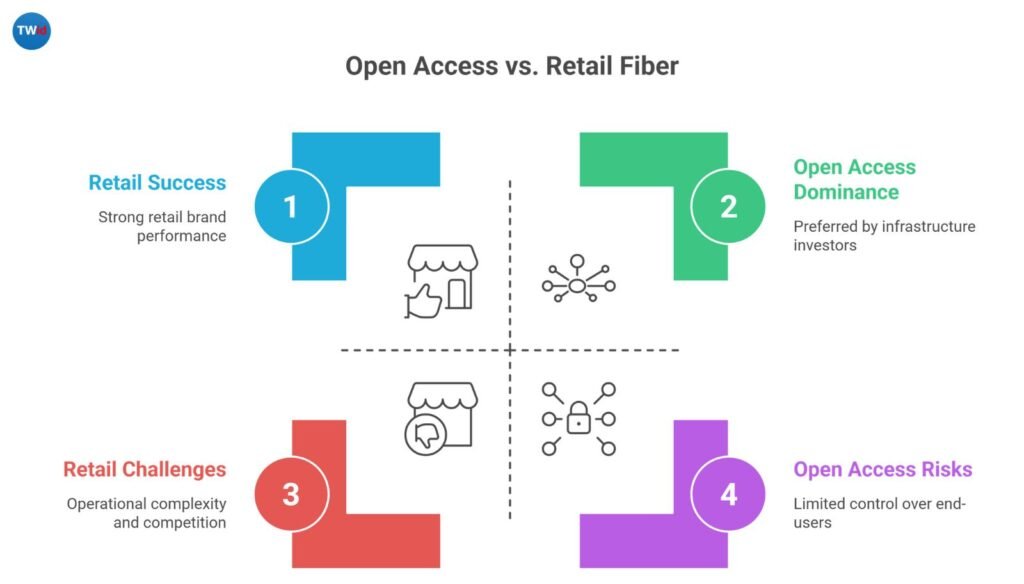

The retail model isn’t without advantages. When it works, per-subscriber margins are higher because the operator captures the full revenue stack — infrastructure fees plus retail pricing. There’s no wholesale discount eating into the economics.

For operators with strong consumer brands, established distribution channels, and the operational muscle to manage customer acquisition and churn at scale, retail can be a powerful model. You own the customer relationship. You control pricing. You dictate the service experience end to end.

But the risk profile is different.

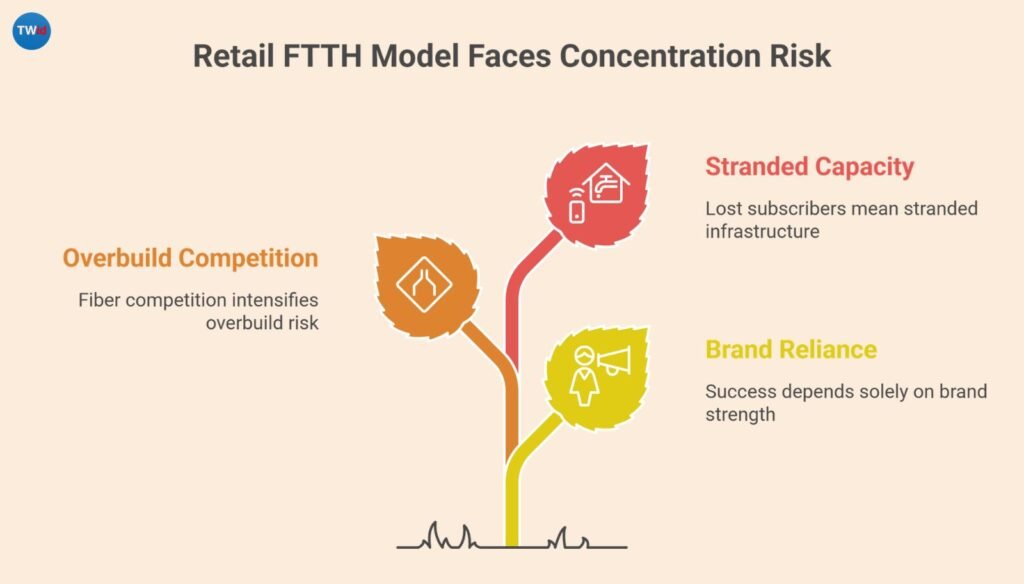

Retail FTTH operators carry concentration risk. You’re betting that your brand alone can sustain enough take-rate to justify the infrastructure investment. In markets where overbuild is increasing — and it is, with fiber competition intensifying rapidly in many regions — that bet becomes harder to win. As EY reported, return minimums for FTTH builds have risen from the 8-10% range in 2021-2022 to 12-15% today, largely driven by higher interest rates and growing competitive overbuild risk (source).

When your only path to monetizing each home is winning the retail customer, every lost subscriber is stranded capacity.

What Investors Actually Prefer — And Why It Matters

Here’s where the valuation gap gets real.

Infrastructure funds, pension capital, and private equity firms have increasingly signaled a preference for wholesale and open access fiber models. The reason is structural: open access revenue profiles resemble utility cash flows — long-term, contracted, and diversified across multiple tenants. That’s the kind of predictable income stream that infrastructure investors are built to underwrite.

UBS noted in its analysis of the FTTH investment landscape that open access structures have become particularly attractive to infrastructure investors because they own the core asset, face minimal concern about competing networks in their territory, and avoid the operational complexity of servicing retail customers directly (source).

The numbers tell the story. Open access fiber entities in Europe have seen enterprise valuations increase substantially — in some cases approaching 10x multiples — while certain vertically integrated telcos have experienced enterprise value contraction over the same period. Wholesale-only fiber models have been cited as generating steady annual returns in the range of 12% to 18%, compared to higher variance outcomes in retail models.

One real-world case from a Scandinavian market illustrates the shift: an electric utility that operated as its own retail ISP for a decade decided to transition to a wholesale open access model. Within three years of the switch, total revenue increased by nearly 40%, staff costs dropped by 25%, and EBITDA margin jumped from 6% to 57%. That’s not a marginal improvement — it’s a fundamental transformation in business economics.

The European Precedent: What Open Access Markets Tell Us

Europe offers the most mature data set for evaluating open access FTTH model performance at scale. Countries with regulated or voluntarily adopted open access frameworks — particularly in Scandinavia, the Netherlands, and parts of Southern Europe — have generally achieved superior infrastructure utilization, faster take-rate ramps, and more competitive pricing for consumers.

Sweden is the standout example. Fiber penetration has grown from roughly 50% to around 95% of households with access to fiber-based broadband, and much of that growth was driven by open access municipal networks where multiple ISPs compete on shared infrastructure.

In markets like Singapore and Italy, where open access fiber plays a prominent role, gigabit-speed packages have become baseline offerings at affordable prices — a direct consequence of the competitive dynamics that open access enables. In markets where a single operator controls both infrastructure and retail, gigabit broadband tends to be positioned as a premium product with significantly higher pricing.

The competitive dynamics differ fundamentally. Open access drives consumer benefit through ISP competition while protecting the infrastructure investor’s revenue — a combination that’s hard to replicate in a vertically integrated model.

For a deeper look at how the utilization and revenue mechanics play out when multiple ISPs operate on the same fiber plant, this analysis of how open-access FTTH networks improve utilization and revenue yield unpacks the financial model in detail.

Where Retail Still Wins — And Where It Doesn’t

Let’s be fair to the retail model. It works well in specific conditions.

If you’re an incumbent with an established consumer brand, deep local market knowledge, and an existing customer base you can migrate onto fiber, retail makes strategic sense. You already have the brand equity, the distribution channels, and the operational infrastructure. Going open access would mean sharing your hard-built competitive advantage with rivals.

Retail also works in markets with limited overbuild risk — dense rural or underserved areas where you’re likely to be the only fiber provider for the foreseeable future. In those contexts, concentration risk is lower because there’s no competing infrastructure to siphon subscribers.

Where retail struggles is in competitive urban and suburban markets where multiple operators are chasing the same homes. The math gets punishing fast: rising build costs, higher cost of capital, and an increasing number of homes served by two or more fiber providers. When your only revenue comes from winning the retail customer, overbuild risk translates directly into stranded CapEx.

Making the Decision: A Framework for Long-Term Value

The open access vs retail decision isn’t about which model is “better” in the abstract. It’s about which model aligns with your capital structure, competitive environment, and long-term strategic ambitions. Here’s a practical framework for thinking through it.

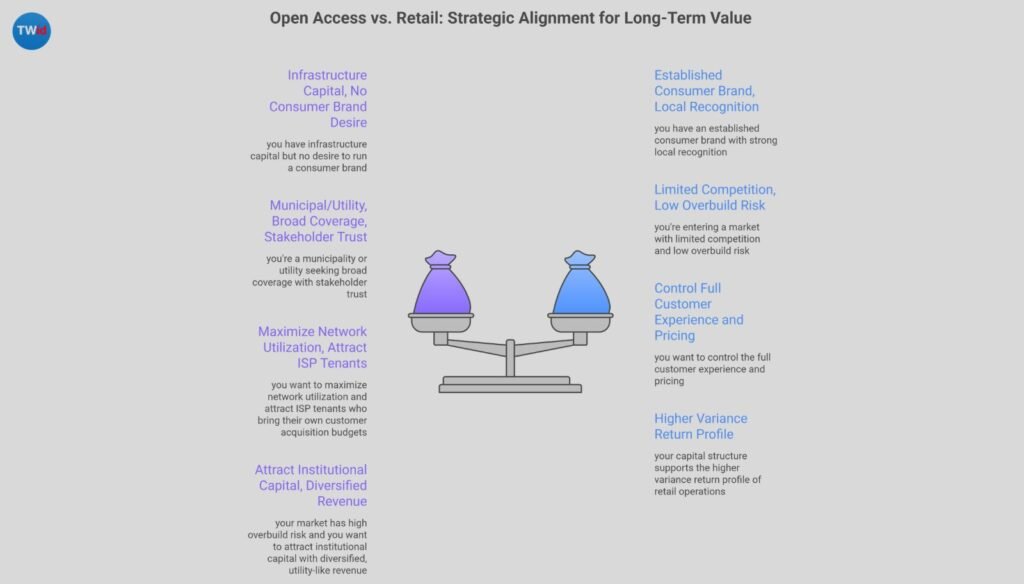

Choose open access if: you have infrastructure capital but no desire to run a consumer brand; you’re a municipality or utility seeking broad coverage with stakeholder trust; your market has high overbuild risk and you want to attract institutional capital with diversified, utility-like revenue; or you want to maximize network utilization and attract ISP tenants who bring their own customer acquisition budgets.

Choose retail if: you have an established consumer brand with strong local recognition; you’re entering a market with limited competition and low overbuild risk; you want to control the full customer experience and pricing; or your capital structure supports the higher variance return profile of retail operations.

Consider hybrid if: you want the control of retail with the upside of wholesale; you can operate as an anchor tenant on your own infrastructure while opening additional capacity to third-party ISPs; or you’re transitioning from a retail model and want to test open access without a full structural shift.

Whatever you choose — commit architecturally from day one. Retrofitting a retail network into an open access platform mid-deployment destroys value and creates operational chaos.

The Bottom Line

The global FTTH market is projected to grow at double-digit rates through the end of the decade. Capital is flowing, competition is intensifying, and the operators who position their networks as high-utilization, investable infrastructure assets will capture disproportionate long-term value.

The open access FTTH model isn’t the right answer for every operator. But the data increasingly suggests it’s the right answer for the market conditions most operators are facing: rising build costs, higher cost of capital, intensifying overbuild, and institutional investors who prefer diversified infrastructure plays over concentrated retail bets.

The question isn’t whether your fiber is good enough. It’s whether your business model is built to extract the maximum value from every strand you’ve deployed.

Start pressure-testing your model against your capital structure, competitive environment, and long-term strategy this quarter. The operators who make this decision with discipline now will be the ones still compounding value a decade from now.

Frequently Asked Questions

What is an open access FTTH model and how does it differ from retail?

An open access FTTH model separates infrastructure ownership from service delivery. A network company builds and maintains the fiber, while multiple ISPs compete to serve customers on the same infrastructure. Retail FTTH bundles everything under one operator — build, operate, and serve. The fundamental difference is who bears the customer acquisition risk and how the network gets monetized.

Why do infrastructure investors prefer the open access FTTH model over retail?

Infrastructure investors favor open access because it produces diversified, contracted revenue streams that resemble utility cash flows. Instead of depending on a single retail brand to win customers, revenue comes from multiple ISP tenants — reducing concentration risk, lowering churn exposure, and creating the kind of predictable income profile that pension funds and infrastructure funds are designed to underwrite.

Can a retail FTTH operator transition to an open access model?

Yes, but it’s expensive and operationally complex if done mid-deployment. The architecture, commercial agreements, and operational workflows are fundamentally different. Operators who anticipate a future move to open access should build with that flexibility in mind from day one — including network design, OSS/BSS infrastructure, and contractual structures. Retrofitting after the fact often destroys more value than it creates.

What take-rates can operators expect under each model?

Single-operator retail networks in competitive urban markets typically achieve take-rates between 30% and 50%. Open access networks with multiple ISPs have reported take-rates ranging from 70% to 90%, because customers are monetized regardless of which retail brand they choose. Higher take-rates translate directly to better infrastructure utilization and faster payback on CapEx.

Is the open access FTTH model only viable in regulated markets?

No. While open access has historically been associated with regulatory mandates in markets like Australia and parts of Europe, an increasing number of operators are adopting it voluntarily as a competitive strategy. In the United States, large telecom companies are exploring joint venture structures that incorporate open access principles — particularly to attract infrastructure capital and reduce overbuild risk in competitive markets.