How Open-Access FTTH Networks Improve Utilization and Revenue Yield

If you’re a fiber operator sitting on a half-built network with a take-rate stuck below 35%, you already know the math isn’t working. The CapEx is sunk, the homes are passed, but the revenue is trickling in too slowly to satisfy your investors. What most operators don’t talk about loudly enough is that the business model — not the network — is often the real constraint.

That’s where open-access FTTH economics changes the conversation entirely.

Open-access isn’t just a regulatory compliance play. For operators who structure it correctly, it’s a deliberate strategy to drive higher network utilization, diversify revenue streams, and ultimately improve yield on a capital-intensive asset. This post breaks down how it works, what the data actually shows, and where operators tend to get it wrong.

The Utilization Problem at the Heart of FTTH Economics

Here’s the uncomfortable reality: most fiber networks are built to serve 100% of homes passed but monetized at a fraction of that capacity. The average take-rate in a competitive urban market sits somewhere between 30% and 50%. That means anywhere from half to two-thirds of your deployed fiber is generating zero revenue on any given day.

Traditional vertically integrated operators — those who build, operate, and retail on their own network — carry the full weight of customer acquisition, churn management, and service delivery on top of infrastructure costs. When take-rates lag, every piece of that stack bleeds margin.

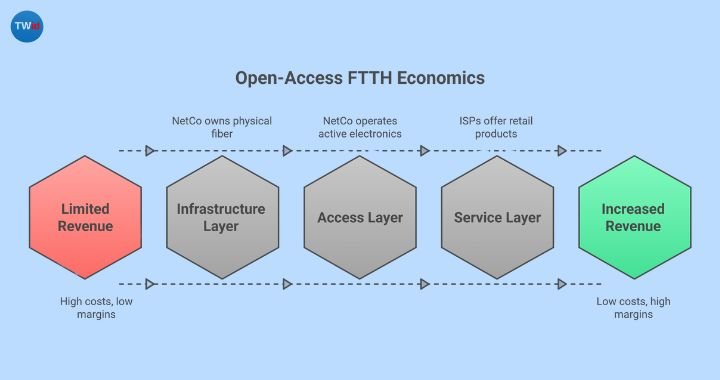

The open-access model separates those layers. The network company (NetCo) owns and operates the physical infrastructure. Multiple service providers (ISPs) ride the network and compete for end-users.

The NetCo generates revenue from wholesale access fees, regardless of which ISP wins the customer. This is the structural shift that makes utilization economics genuinely different.

What Open-Access FTTH Economics Actually Means

Before we get into the revenue mechanics, let’s be precise about what we’re talking about. Open-access FTTH economics refers to the financial dynamics created when a fiber infrastructure is opened to multiple competing service providers under a wholesale access model.

The three-layer model looks like this:

- Infrastructure Layer: Physical fiber, ducts, passive optical components — owned by the NetCo

- Access Layer: Active electronics, network management, SLAs — operated by the NetCo or a neutral operator

- Service Layer: ISP retail products, customer billing, marketing — owned by competing service providers

The revenue model for the NetCo is wholesale access fees per subscriber activated, plus potentially dark fiber leases and enterprise connectivity revenues. Because the cost of adding a new tenant onto an existing network is minimal, each additional ISP that joins the platform translates directly to higher margin — incremental revenue without proportional incremental cost.

This is why institutional investors are increasingly drawn to the model. Open-access fiber networks have gained significant momentum in the U.S. as a capital-efficient approach, with national wireless operators and infrastructure funds treating it as a path to infrastructure-style yields rather than traditional telecom returns.

If you’re evaluating whether to pursue this structure, it’s worth reading our earlier breakdown on the strategic differences between retail, wholesale, and open-access FTTH models first — the structural choice upstream determines everything about how revenue yield develops downstream.

How Multi-Tenant Networks Drive Higher Utilization

The utilization math shifts substantially when multiple ISPs compete on the same network. Here’s why.

In a single-operator retail model, the operator competes for a customer and either wins or loses. If the customer goes with a competitor on a different network, the operator’s infrastructure sits dark on that home.

In an open-access model, the outcome is different: if a competing ISP acquires that same customer over your network, the NetCo still earns a wholesale fee. The customer is monetized regardless of retail brand preference.

This structural shift transforms the competitive landscape from zero-sum to collaborative at the infrastructure level. More ISPs competing on the network means more customer acquisition activity — funded by the ISPs — which directly drives take-rate on the NetCo’s infrastructure.

UTOPIA Fiber in Utah is the clearest proof point in the U.S. market. The 20-city municipal consortium now hosts 15 competing ISPs across more than 100,000 households and has been operating profitably, with service options ranging from entry-level broadband to multi-gigabit tiers.

The competitive tension between ISPs drove both take-rate growth and pricing competitiveness — without the NetCo absorbing customer acquisition cost.

The European experience makes the same case at scale. Countries with mandated open-access frameworks have consistently achieved higher penetration rates. Spain, with one of the most competitive open-access environments in Europe, has reached a take-up rate above 90% — a figure that vertically integrated operators in less competitive markets struggle to approach.

Revenue Yield: The Case for Wholesale-Plus Models

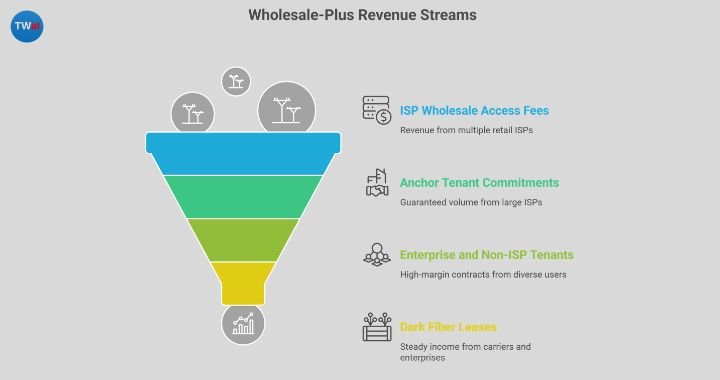

Pure wholesale is one model. But the most financially attractive open-access structures for private operators are what practitioners are calling “wholesale-plus” — where the NetCo earns layered revenues across multiple streams.

Consider what a well-structured open-access network can monetize:

Tier 1 — ISP Wholesale Access Fees Per-subscriber fees from multiple retail ISPs. The more ISPs, the more diversified and resilient this revenue stream becomes. No single ISP departure collapses the revenue base.

Tier 2 — Anchor Tenant Commitments Large ISPs or carriers commit to a minimum take volume in exchange for preferred wholesale terms. This de-risks the early ramp period and supports the initial debt structure. The AT&T and BlackRock GigaPower joint venture uses this logic explicitly — anchor-tenant economics underwrite the build, with additional ISP tenants improving yield over time.

Tier 3 — Enterprise and Non-ISP Tenants Open-access infrastructure can be leased to enterprises, utilities, government agencies, and wireless carriers for backhaul. These are often high-margin, long-duration contracts that are completely uncorrelated to residential broadband churn. Ubiquity, one of the private-sector open-access operators, describes this as making networks “three-dimensional” — multiple uses and multiple providers across the same last-mile infrastructure.

Tier 4 — Dark Fiber Leases Carriers and enterprises willing to manage their own electronics can lease dark fiber strands, providing steady passive income with near-zero operational overhead for the NetCo.

This multi-tier revenue structure is why investor-backed NetCos are increasingly repricing their equity stories to infrastructure-style valuations — CPI-linked fees, long-life cash flows, and diversified revenue bases. It’s also why the model aligns well with growing ARPU strategies. For operators already pursuing ARPU optimization on a retail model, understanding how fiber broadband providers can grow revenue per user without increasing churn becomes directly applicable when transitioning toward wholesale structures.

What the Data Shows About Open-Access Network Performance

The global fiber market context matters here. The FTTH market was valued at $56 billion in 2024 and is projected to reach $110 billion by 2030, growing at 12.4% annually. In that growth environment, the competition for subscribers — and for capital — is intensifying rapidly.

The operators who position their networks as neutral infrastructure platforms will attract both ISP tenants and institutional capital more easily than those locked into a single retail brand. Infrastructure capital has a clear preference for diversified, long-duration revenue streams over concentrated retail broadband bets.

The European precedent backs this up at the market level. Countries with regulated open-access frameworks have generally achieved superior utilization, faster take-rate ramp, and stronger competitive pressure that benefits the underlying infrastructure economics.

Sweden’s Stokab (a wholesale-only dark fiber provider in Stockholm) has operated for over two decades as a model of how infrastructure separation creates both investment efficiency and market resilience.

In the U.S., where open-access is not mandated, the adoption is being driven by economics rather than regulation. The current interest rate environment — which pushed minimum FTTH build return requirements from roughly 8–10% in 2021 to 12–15% today — makes the diversified revenue logic of open-access even more compelling for investors who need infrastructure-level certainty.

Where Operators Get the Open-Access Model Wrong

Open-access FTTH economics only work when the execution matches the structure. The most common failure points:

Operational Standardization Is Non-Negotiable The speed at which ISPs can be onboarded — from order to revenue — is one of the defining operational metrics of a NetCo. Without standardized processes and automated provisioning, each new ISP becomes a custom integration project. That kills the scalability that makes the model work.

Anchor Tenant Selection Matters More Than You Think Starting with a weak or uncommitted anchor ISP leaves the NetCo exposed during the ramp period. The best-performing open-access networks enter the market with an anchor-tenant commitment that absorbs a meaningful floor of wholesale fees before the first additional ISP is onboarded.

Pricing Architecture Has to Be Transparent ISPs will only commit to an open-access network if they can model their margins with confidence. Opaque or discretionary wholesale pricing creates distrust and reduces the number of ISPs willing to compete on the platform.

Infrastructure Quality Drives Long-Term Retention The NetCo’s customer is the ISP, not the end-user. But end-user experience is the ISP’s primary SLA requirement. If network reliability, speed consistency, or provisioning quality degrades, ISPs churn off the platform. The infrastructure layer must be operated to enterprise standards.

Is Open-Access the Right Model for Your Network?

Not every fiber network benefits from the open-access structure. The model performs best when:

- The serviceable market has competitive DSL or cable infrastructure that multiple ISPs can displace

- Sufficient ISP demand exists — or can be cultivated — to populate the wholesale marketplace

- The operator is willing to forgo retail brand equity in exchange for infrastructure yield

- The capital structure allows for a longer ramp-up before multi-ISP revenues normalize

In markets where only one ISP is likely to ever operate on the network, the open-access structure adds complexity without meaningful revenue benefit. The model pays off when the platform genuinely attracts multiple tenants. That’s what converts underutilized fiber into a revenue-compounding infrastructure asset.

For executives evaluating the transition, the critical question isn’t whether open-access is theoretically superior — the economics generally support it in the right market conditions. The question is whether your current organization, operational stack, and capital structure are positioned to execute it well.

5 Frequently Asked Questions on Open-Access FTTH Economics

1. What is the main revenue difference between an open-access FTTH network and a traditional retail fiber model?

In a traditional retail model, the operator earns revenue only from the customers it directly acquires and retains. In an open-access model, the NetCo earns wholesale fees from every ISP tenant that activates subscribers on the network — regardless of which ISP wins the customer. This diversifies revenue and reduces dependence on any single retail take-rate.

2. Does open-access FTTH always require a regulatory mandate to be viable?

No. While open-access has historically been associated with regulated European markets, private operators and institutional investors in the U.S. are increasingly adopting it for purely economic reasons. The model reduces customer acquisition costs for the NetCo, diversifies revenue, and attracts infrastructure-style capital — independent of any regulatory requirement.

3. How does open-access affect network utilization specifically?

By allowing multiple ISPs to compete for subscribers over the same physical infrastructure, open-access aligns the competitive incentives of ISPs with the NetCo’s utilization goals. More ISPs mean more sales activity, more customer acquisition, and higher overall take-rate — without the NetCo absorbing the retail acquisition cost.

4. What are the biggest risks of transitioning to an open-access or wholesale model?

The primary risks are operational complexity (provisioning multiple ISPs requires standardized systems), anchor tenant dependency (early revenue depends heavily on a committed first ISP), and margin compression in wholesale pricing if the operator underprices access to attract tenants. Getting the wholesale pricing architecture right from the start is critical.

5. What financial metrics should executives track to evaluate open-access network performance?

The key metrics are: wholesale revenue per home passed (not just per subscriber), ISP tenant count and diversity, time-to-revenue per new ISP onboarded, network utilization rate across homes passed, and EBITDA margin by revenue tier. Infrastructure investors specifically focus on revenue durability and diversification — the number of ISP tenants and their combined revenue floor is as important as overall take-rate.

The Bottom Line

Open-access FTTH economics isn’t a theory — it’s a model that’s been stress-tested in some of the world’s most competitive fiber markets and is gaining serious traction with sophisticated capital. The core logic is straightforward: build the infrastructure once, open it to multiple service providers, and earn diversified revenue on every subscriber regardless of which retail brand wins the home.

For FTTH executives navigating a market where build costs are rising, return hurdles are tightening, and competition is intensifying, the utilization and revenue yield advantages of open-access deserve serious strategic consideration.

Ready to evaluate whether an open-access model fits your network and market? Contact us to discuss how the right content strategy can position your organization at the forefront of this shift.